Meredythe | March 31, 2026 | Blog

A car crash in Austin can leave you overwhelmed and unsure about what happens next. Insurance companies, liability questions, and medical bills pile up quickly, making it hard to know your rights.

At Heaton Injury Law, PLLC, we help injured Austinites navigate Austin car crash claims step by step. This guide walks you through what you need to do now and what mistakes to avoid later.

Understanding Austin Car Crash Claims

What Types of Claims Can You Actually File in Texas

In Texas, car crash claims follow two distinct paths, and understanding which one applies to your situation determines everything about how your case moves forward. The first path is a claim against the at-fault driver’s liability insurance, which covers their legal responsibility for injuries and property damage they caused. Texas law requires all drivers to carry minimum liability coverage of $30,000 per person and $60,000 per accident for bodily injury, plus $25,000 for property damage. The second path involves your own insurance policy, which covers you in two separate ways. If you carry uninsured / underinsured motorist coverage, your own insurance policy may kick in to cover your losses where the other driver’s liability policy based on their available liability coverage. Second, your own insurance will cover you regardless of fault through collision coverage for vehicle damage and medical payments coverage or personal injury protection for medical expenses and lost wages. Many injured Austinites overlook their own policy options and focus only on the other driver’s insurance, which can cost them thousands in uncompensated losses if that driver is uninsured or underinsured.

How Fault Gets Determined in Austin Crashes

Texas follows a modified comparative negligence rule, meaning you can recover damages even if you were partially at fault, as long as you were not more than 50 percent responsible for the crash. Insurance adjusters assign fault percentages based on police reports, witness statements, vehicle damage patterns, and traffic laws violated at the scene. The problem is that adjusters work for insurance companies and are trained to minimize payouts, so their initial fault determination often favors their insured driver. Austin police crash reports carry significant weight in these determinations, and you should obtain a copy immediately after the crash by requesting the case number and filing a records request with the Austin Police Department. Surveillance footage from nearby businesses or traffic cameras can override an adjuster’s narrative if it shows clearly who caused the collision, so document every camera location at the scene. If the other driver received a traffic citation at the scene, that citation creates strong evidence of fault and substantially improves your claim value.

Coverage Layers That Protect You

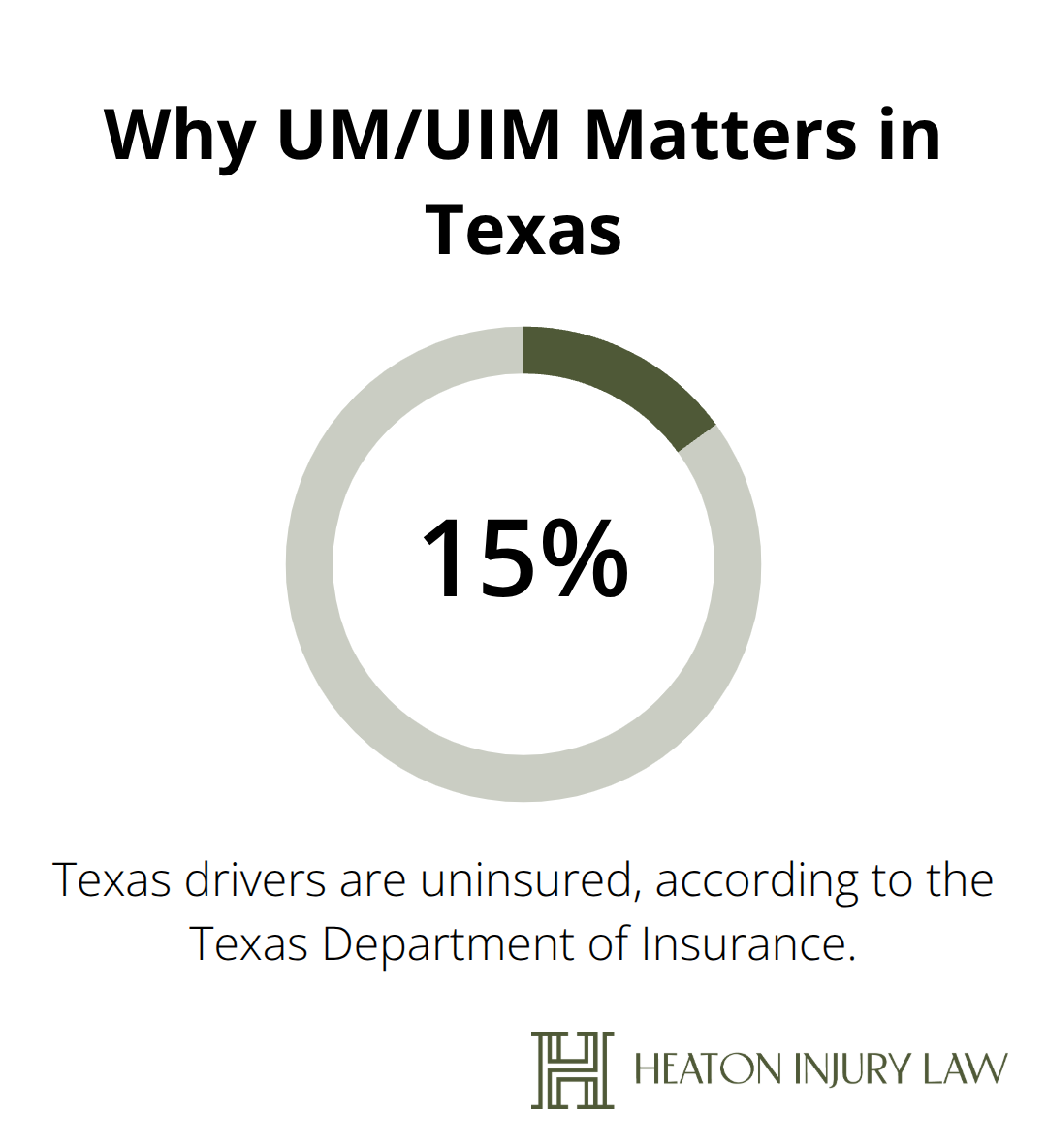

Most injured people in Austin have access to multiple insurance coverages they never use because they do not understand them. Uninsured / underinsured motorist coverage (UM / UIM) protects you when the at-fault driver has no insurance or insufficient coverage to pay your full damages. Texas does not require drivers to carry uninsured motorist coverage, but approximately 15 percent of Texas drivers are uninsured according to the Texas Department of Insurance, making this protection essential.

Medical payments coverage on your policy pays hospital bills and doctor visits regardless of fault, and using this coverage does not increase your premium or count as a claim against your policy limits. If you have a job, income protection through your policy’s medical payments or personal injury protection coverage compensates you for lost wages while you recover, and this money comes from your own insurer, not from negotiating with the other driver. Rental car coverage through your policy pays for a temporary vehicle while yours is being repaired, and you should use this benefit immediately rather than absorbing rental costs yourself.

Now that you understand the claim types and coverage available to you, the immediate actions you take at the crash scene will determine whether you can actually prove your case and recover what you deserve. If you have been injured in a crash, contact a skilled Austin personal injury lawyer to discuss your options and protect your rights.

Immediate Steps After a Car Crash in Austin

Most injured people waste this critical window making preventable mistakes. If no one is seriously injured, you should move both vehicles to the side of the road immediately to prevent additional collisions and clear traffic, then turn on hazard lights. You must call Austin Police Department for any crash involving injuries, hit-and-run situations, or significant property damage-do not skip this step thinking minor crashes do not matter, because the police report becomes the official record that insurance companies and courts rely on.

Protect Yourself at the Scene

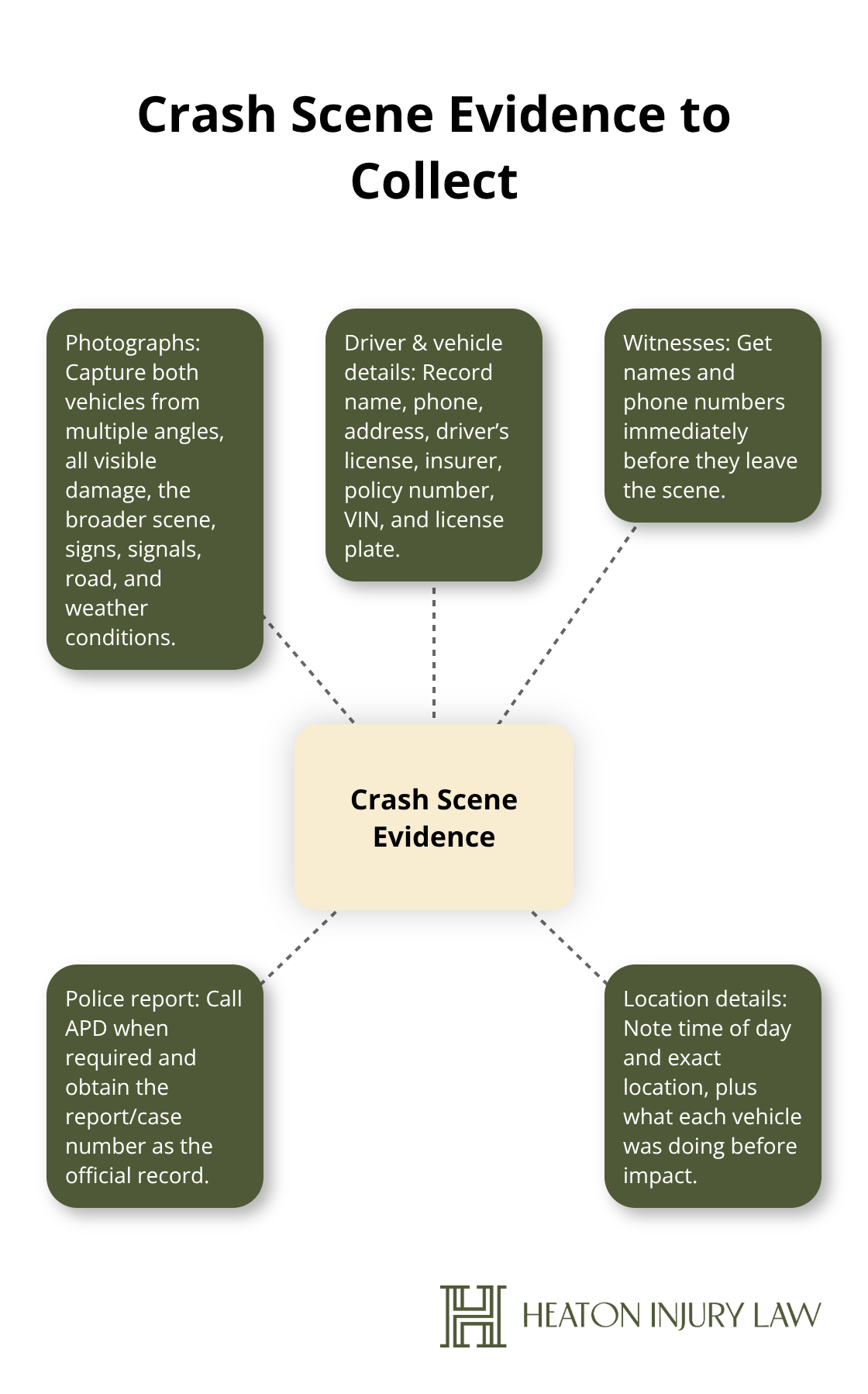

While waiting for police, you need to stay calm and avoid admitting fault, apologizing, or making statements about who caused the crash, even if you feel responsible; anything you say at the scene can be used against you later. You should collect the other driver’s name, phone number, address, driver’s license number, insurance company name, policy number, and vehicle information including the VIN and license plate. You must photograph their insurance card and driver’s license with your phone, then photograph their vehicle from multiple angles showing all damage.

You should also photograph your own vehicle damage, the accident scene from different positions, street signs, traffic signals, road conditions, and weather conditions-these photos become critical evidence when the other driver’s insurance company disputes your account of what happened.

Gather Witness Information and Scene Details

You need to talk to any witnesses at the scene and write down their names and phone numbers immediately; witnesses often disappear, and their statements can override disputed facts later. You should document the time of day, exact location, weather conditions, and what each vehicle was doing before impact in a note on your phone while details are fresh. This information creates a contemporaneous record that proves more reliable than your memory weeks or months later when the claim process unfolds.

Seek Medical Attention Without Delay

You cannot wait to seek medical attention hoping you will feel better tomorrow. Texas injury claims require medical documentation to prove your injuries. Delaying treatment gives insurance companies ammunition to argue your injuries are not serious. You should get examined by a doctor or visit an urgent care clinic within 24 hours of the crash, even if you feel only minor pain, because some injuries like whiplash and internal injuries develop over hours or days and early medical records prove the connection between the crash and your injuries. Keep a record of every provider you saw for your accident related injuries so complete records and medical bills may be requested.

Report the Crash and Communicate Strategically

You should report the crash to the other driver’s insurance company and your own insurance company within the timeframe specified in your policy, typically within 24 to 72 hours, and provide them with the police report number and the other driver’s insurance information. When you speak with any insurance adjuster, you must stick to the facts and avoid speculation; tell them what happened, but do not discuss settlement or accept any payment offer without understanding your full damages. Do not provide a recorded statement unless it is mandated by your policy. You need to request the adjuster’s name and direct contact information, document the date and time of every conversation. If the other driver is uninsured or underinsured, you must file a claim with your own insurer under your uninsured or underinsured motorist coverage immediately, as these claims have strict deadlines in Texas that can eliminate your right to recover if missed.

The actions you take in these first days set the foundation for your entire claim, but many injured people still make critical errors even after handling the immediate aftermath correctly. Understanding which mistakes reduce your claim value helps you avoid the traps that cost injured Austinites thousands in lost recovery. If you need guidance navigating these steps, contact a skilled Austin personal injury lawyer who can protect your rights from the start.

Common Mistakes That Reduce Your Claim Value

Insurance adjusters count on injured people to sabotage their own claims through panic, impatience, and misinformation. The three most destructive errors happen in the days and weeks immediately after your crash, and each one directly reduces what you ultimately recover. Understanding why these mistakes happen and how to avoid them protects thousands of dollars in your settlement.

Admitting Fault or Apologizing at the Scene

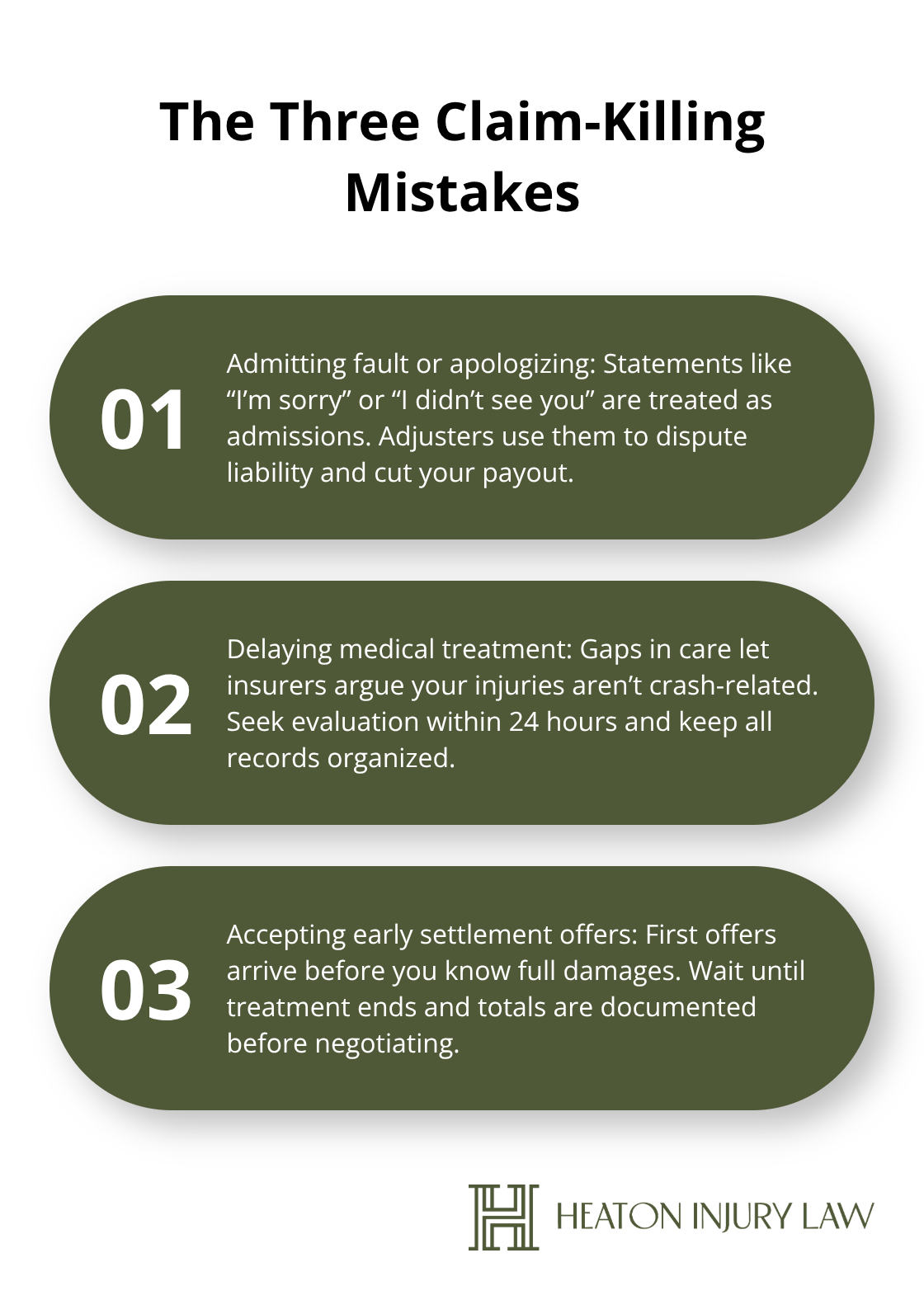

The first mistake is saying anything at the scene that sounds like an admission of fault, and this includes apologies. When you tell the other driver “I’m sorry” or say “I didn’t see you coming,” you hand the insurance adjuster a recorded statement or witness account that contradicts your claim later. Insurance companies train adjusters to interpret these statements as admissions of liability, and they will use them to argue you caused the crash. Texas courts allow these statements as evidence, and the other driver’s insurer will absolutely present them to minimize their client’s responsibility.

Do not apologize for anything at the scene, do not speculate about what happened, and do not make any statements about fault, even if you genuinely believe you caused the crash. Stick to factual observations: “I was traveling at the posted speed limit. The traffic light was green. The other vehicle struck my driver’s side door.” Nothing more. If an adjuster calls and asks leading questions about fault, answer only what they ask and volunteer nothing beyond the specific facts.

Delaying Medical Treatment Destroys Your Evidence

The second mistake that destroys claim value is waiting to seek medical treatment or skipping it entirely because you hope you will feel better tomorrow. Insurance adjusters rely on gaps in medical records to argue your injuries are not related to the crash or are not as serious as you claim, and a two-week delay between the crash and your first doctor visit creates exactly the opening they need. Treatment delays significantly reduce settlement amounts because adjusters attribute gap periods to injuries that developed independently of the crash.

Medical documentation from the first 72 hours after impact carries exponential weight compared to records created weeks later, and this timing difference can cost you tens of thousands in reduced recovery. You should seek medical evaluation within 24 hours even if you feel minor soreness, because whiplash, internal injuries, and concussions often develop over the first 48 to 72 hours.

Accepting Early Settlement Offers Before You Know Your Damages

The third claim-killing mistake is accepting an early settlement offer from the other driver’s insurance company without understanding your full damages. Insurance companies send these offers deliberately before you know the extent of your injuries, before you finish treatment, and before you understand your lost wages and long-term medical needs. Accepting their first offer typically means you recover 30 to 50 percent less than your claim is actually worth because you agreed to a number without complete information.

Most insurance companies speak to you on a recorded telephone line. Even discussing a settlement offer verbally over the phone, with no written documentation, may be used against you by the insurance company to try to hold you to an early settlement when one was not necessarily intended.

Once you accept and sign a settlement release or commit to a verbal settlement offer, you forfeit all rights to additional recovery even if your injuries worsen or require future surgery. Do not engage with settlement discussions until you have completed medical treatment, compiled all medical bills and records, calculated your lost wages with documentation from your employer, and understood whether your injuries will require ongoing care. This comprehensive approach protects your financial recovery and prevents you from settling prematurely.

Final Thoughts

Austin car crash claims succeed or fail based on decisions you make in the first hours and days after impact. You now understand the three claim types available to you, the immediate actions that protect your evidence, and the mistakes that destroy settlement value. Move vehicles to safety, call police, photograph everything, seek medical care within 24 hours, report to your insurer, and never accept early settlement offers before your treatment ends and your damages are fully documented.

Your recovery depends on treating this process as seriously as your injuries deserve. Many injured Austinites navigate claims alone and settle for far less than they should because they lack insider knowledge of how insurance companies operate. The adjusters assigned to your case are trained professionals working to minimize payouts, and they count on injured people to make preventable mistakes under stress and pain.

If your injuries are significant, if the other driver is uninsured or underinsured, or if the insurance company is disputing fault or delaying payment, contact us for a free consultation. We at Heaton Injury Law, PLLC can review your case, explain your options, and handle negotiations so you can focus on healing. Your right to full compensation is worth protecting, and we are here to fight for it.

The information provided in this blog is for general informational purposes only and does not constitute legal advice. Every case is unique, and laws may vary by jurisdiction. Reading this content does not create an attorney-client relationship. For guidance specific to your situation, please consult with a qualified personal injury attorney licensed in Texas.

Artificial intelligence may have been used to assist in generating some text or images in these articles.