Meredythe | April 21, 2026 | Blog

Auto collisions in Austin happen fast, but the aftermath moves slowly-especially when insurance companies are involved. We at Heaton Injury Law, PLLC know that initial settlement offers rarely reflect what your claim is actually worth.

This guide walks you through how insurers operate, what steps protect your interests, and when legal representation makes the real difference in Austin auto collision claims.

How Insurers Minimize What They Pay You

The Investigation Playbook

Insurance companies operate with a clear financial incentive: pay out as little as possible on every claim. In Austin, adjusters follow a predictable playbook designed to reduce claim value before you fully understand what happened. Within 24 to 48 hours of your accident, an adjuster is assigned and begins pulling the police report, which often sets the baseline for fault determination. However, the insurer’s investigation extends far beyond the officer’s initial findings. Adjusters examine weather conditions, road hazards, citations, and witness statements to build a narrative that favors their position. Inconsistencies between your account and the police report can severely damage your credibility, even if those inconsistencies involve minor details or do not accurately reflect your statements to the investigating police officer.

Recorded Statements and Social Media Surveillance

One common tactic involves requesting a recorded statement early in the process, before you’ve had time to consult with anyone or fully assess your injuries. Texas law does not require you to provide a recorded statement for a third-party claim, yet insurers pressure claimants into these conversations knowing that casual language, hesitation, or any statement about pre-existing conditions can be twisted later to minimize payout. Another strategy involves social media surveillance. Insurers routinely monitor your posts for evidence that contradicts your injury claims-a photo at a restaurant, a tagged location at a gym, or even a casual comment can be weaponized against you. Setting your accounts to private or pausing activity during the claims process protects you from this tactic.

Damage Assessments and Lowball Offers

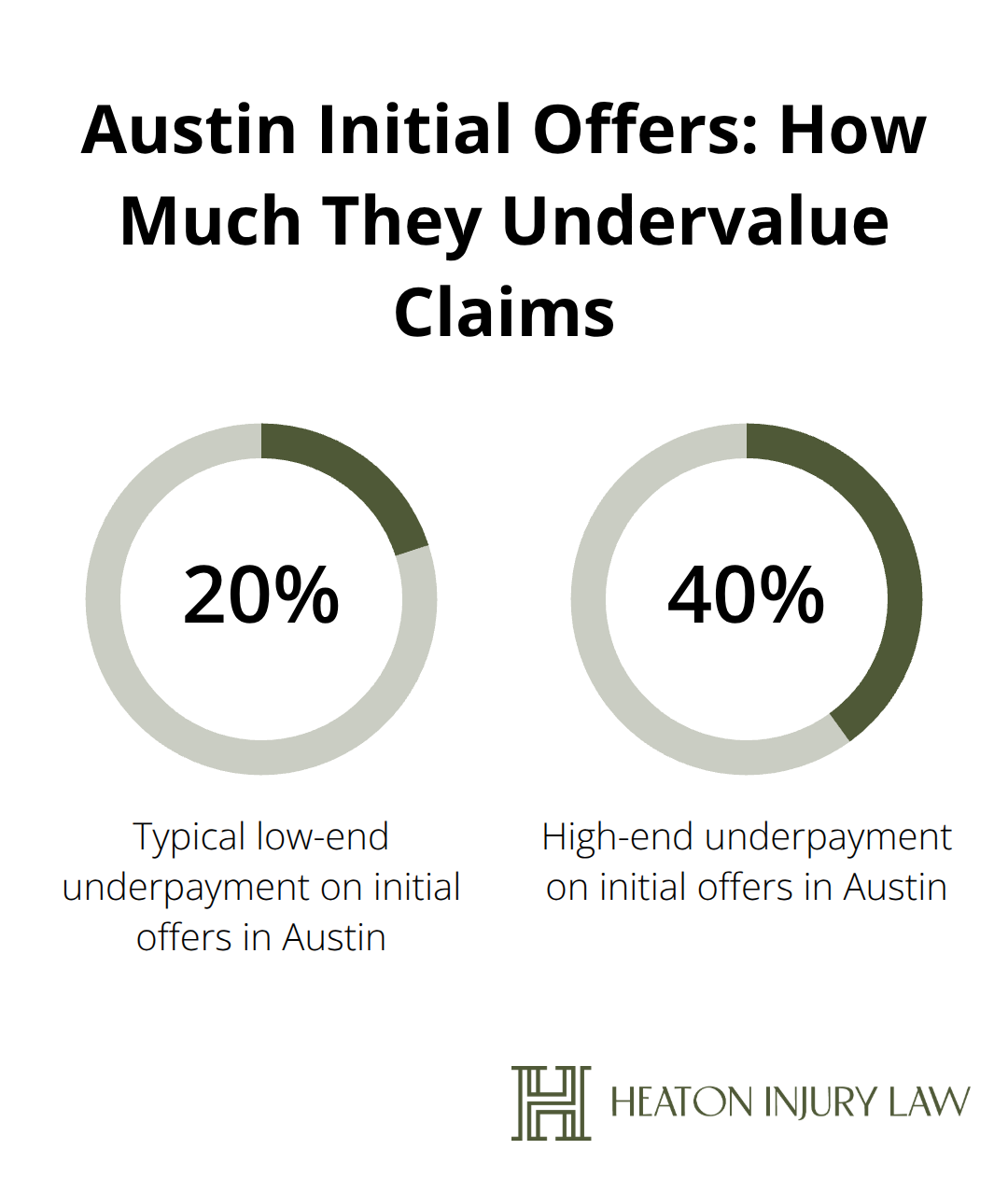

Damage assessments represent another pressure point where insurers cut corners. They may use outdated repair estimates or incorrect car sales comparables to underpay your car’s actual repair costs. If repair costs exceed the initial estimate, the shop provides a new estimate, but insurers sometimes resist approving the higher amount without valid justification. Initial settlement offers in Austin typically come in at 20 to 40 percent below fair value, intentionally low to test whether you’ll accept quickly. The insurer knows that financial pressure (mounting medical bills, rental car costs, lost wages) can push injured claimants to settle prematurely before reaching maximum medical improvement.

Timeline Pressure and Delay Tactics

This is where the timeline becomes critical. Texas law requires insurers to acknowledge claims within 15 days and to accept or deny them within 15 business days of receiving complete documentation. Delay itself functions as a tactic. Extended delays without explanation apply financial pressure and can jeopardize your ability to pursue a lawsuit, since Texas personal injury claims must be filed within two years. Medical records receive intense scrutiny during this process. Insurers examine ER reports, initial treating notes, imaging results, physical therapy records, and any gaps in treatment. They look for ammunition to argue that your injuries aren’t causally related to the accident or that pre-existing conditions explain your symptoms. Independent Medical Examinations arranged by the insurer often involve doctors who spend minimal time with you before concluding you’re fine-a red flag that signals bias. You have rights during an IME: you can request that the examination be recorded, bring a witness, and obtain a copy of the report.

Background Checks and Investigation Intensity

Background checks and prior claims history also factor into investigation intensity. Insurers access CLUE reports, ISO databases, LexisNexis records, and DMV driving records. Multiple prior claims may trigger tighter scrutiny and skepticism of your current claim, even if those prior incidents were legitimate. Understanding these tactics positions you to recognize when an insurer crosses the line from standard investigation into bad-faith practices-a distinction that becomes important when you consider whether legal representation can strengthen your position.

What to Document at the Accident Scene

Photograph Everything at the Scene

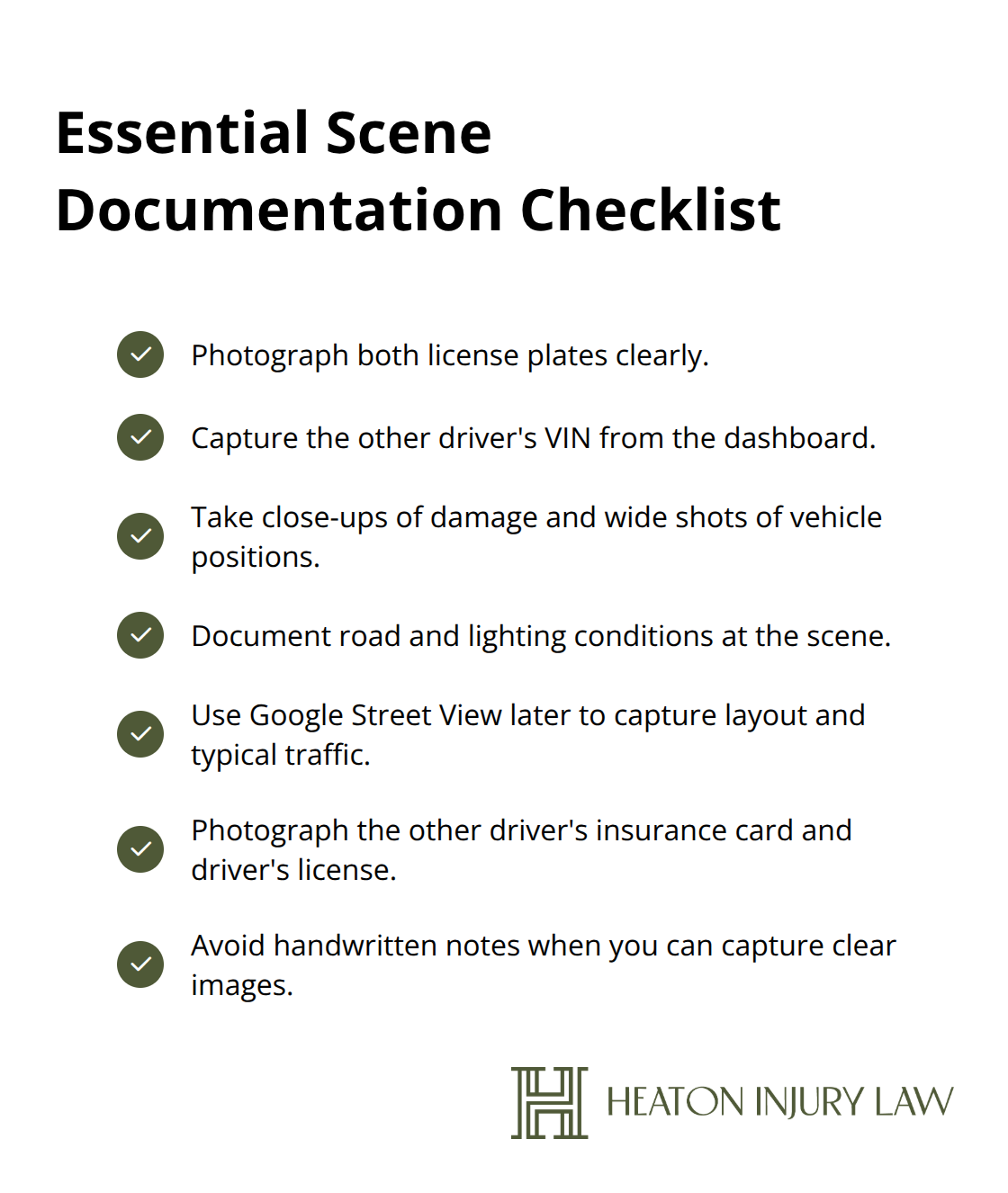

The first hours after a collision determine whether you’ll have leverage in your claim or be left scrambling to reconstruct details months later. Photographs matter more than your memory. Take images from multiple angles of both vehicles, focusing on the point of impact, all visible damage, skid marks, debris, road conditions, traffic signals, and street signs that show the location context. Shoot the license plates clearly, the other driver’s vehicle identification number on the dashboard, and the surrounding area to establish whether the road was wet, icy, or poorly lit. Get close-ups of damage and wide shots showing vehicle positioning. If you can safely access the scene later, Google Street View helps document the location’s layout and typical traffic patterns, which adjusters use to assess fault. Photograph the other driver’s insurance card or better yet, declarations page if available, and driver’s license directly rather than writing information by hand, since handwritten details introduce transcription errors that insurers exploit.

Capture Property Damage Beyond Vehicles

If property damage extends beyond vehicles-damage to a fence, mailbox, or storefront-photograph that damage and note the exact date and time you first observed it, along with weather conditions. This specificity prevents adjusters from claiming the damage occurred at a different time or was pre-existing. Document every detail with precision, as vague or incomplete records give insurers room to dispute what actually happened.

Collect Witness Information at the Scene

Witness statements carry enormous weight because they’re independent of your account, yet most people fail to collect them at the scene. Approach anyone who saw the collision and ask for their full name, phone number, email, and what they observed about how the accident happened. Ask specifically: Did they see which vehicle entered the intersection first? What was the traffic signal color? Did either driver brake or accelerate? Write down their answers verbatim rather than paraphrasing. Insurers interview witnesses independently, and if a witness later tells the insurer something different from what you recorded, your credibility suffers. If a witness is reluctant to provide information, ask for just their phone number and offer to follow up later.

Report to Police and Your Insurer Promptly

Report the accident to police immediately if anyone is injured, the other driver fled, or significant damage occurred-Texas Transportation Code Section 550.062 requires crash reports for certain injury or damage thresholds. Obtain the police report number at the scene and follow up within 7-10 days to get a copy, since the officer’s determination of fault heavily influences the insurer’s investigation. Contact your insurance company within 24 hours, not days. When you call, document the date, time, adjuster’s name, and the specific details you discuss. Texas law requires insurers to acknowledge your claim within 15 days, so prompt reporting starts the clock on their legal obligations.

Protect Yourself During Initial Statements

Do not provide a recorded statement to the other driver’s insurer without consulting an attorney first-you have no obligation to do so under Texas law, and anything you say can be used against you to reduce your payout. This early caution about recorded statements connects directly to understanding when legal representation becomes necessary to protect your interests and navigate the claims process effectively.

Your Rights Under Texas Negligence Law

How Comparative Negligence Affects Your Recovery

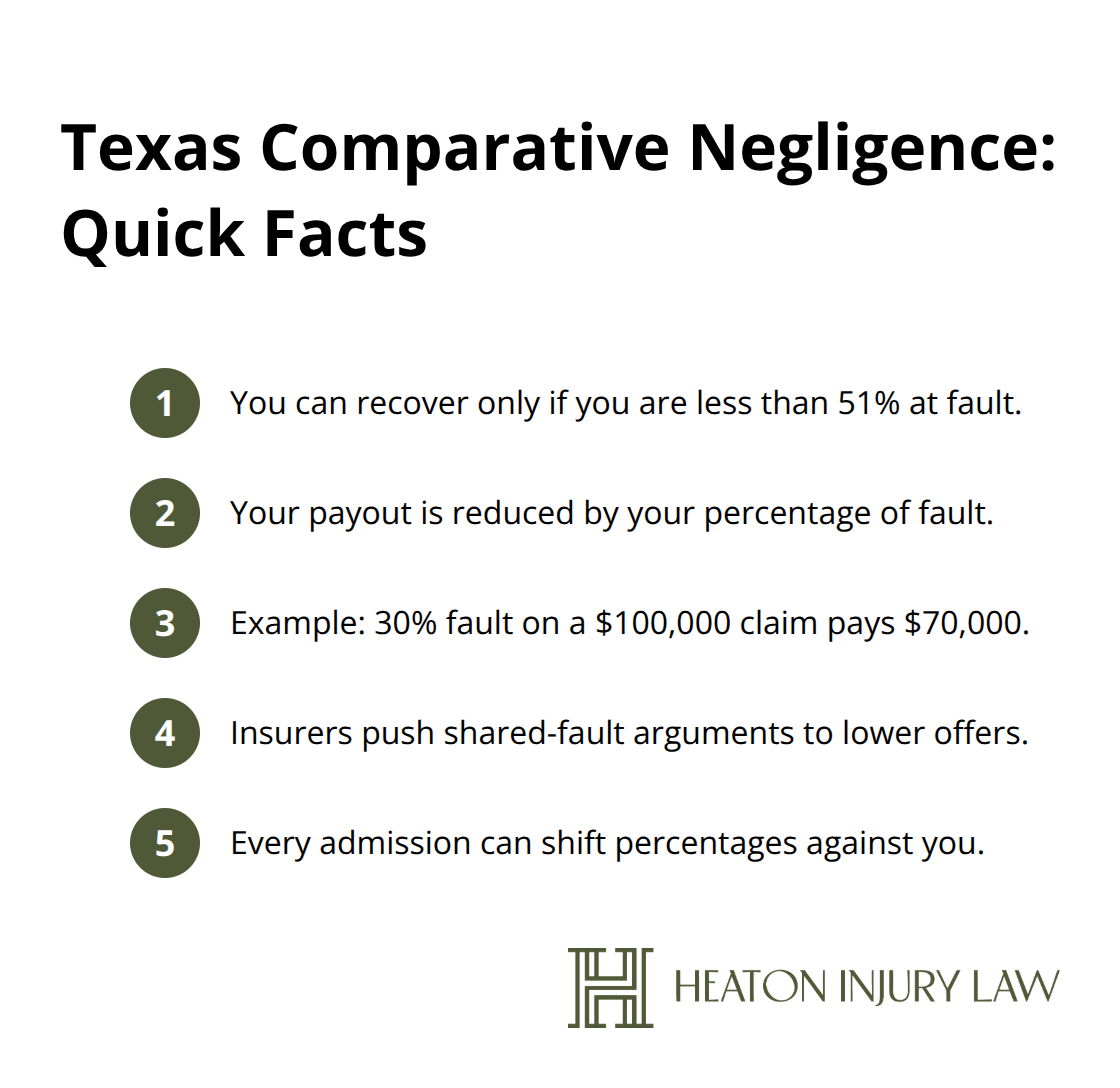

Texas follows a modified comparative negligence rule that directly affects how much compensation you can recover, regardless of how strong your injuries appear. Under Texas Civil Practice & Remedies Code Section 33.001, you can recover damages even if you’re partially at fault for the collision, as long as you’re less than 51 percent responsible. However, your recovery amount is reduced by your percentage of fault. If you’re found 30 percent at fault and your claim is worth $100,000, you recover $70,000. This rule creates enormous leverage for insurers during settlement negotiations because they’ll argue your actions contributed to the accident to lower their payout obligation.

How Adjusters Use Fault Arguments Against You

Adjusters scrutinize every detail of your account for any admission or inconsistency that suggests shared fault. When the police report indicates the other driver violated a traffic law (running a red light, failing to yield, speeding), that citation strengthens your position significantly because it establishes the other driver’s negligence as a matter of public record. Conversely, if the police report cites you for a violation, the insurer will weaponize that citation to argue comparative fault applies. This is why your initial actions at the scene matter: if you admitted fault, apologized, or made statements suggesting you contributed to the accident, those words will resurface in the adjuster’s file and reduce your settlement offer. Texas law doesn’t require you to explain yourself to the other driver’s insurer, yet most people do exactly that without understanding the consequences. The comparative negligence rule means fault determination isn’t binary; it’s a percentage fight where small admissions compound into reduced payouts.

When You Need Legal Representation

Determining whether you need legal representation depends on claim complexity, injury severity, and the insurer’s willingness to negotiate fairly. If your injuries are minor, the damage is clearly the other driver’s fault, and the insurer’s initial offer covers your actual losses without dispute, you can handle the claim yourself. However, serious injuries, disputed liability, multiple parties, commercial vehicles, underinsured or uninsured drivers, or initial offers substantially below fair value signal that legal representation strengthens your outcome significantly. An attorney brings trial readiness to settlement negotiations because adjusters know that refusing a fair offer risks a jury verdict far exceeding their settlement authority.

The Two-Year Deadline and Statute of Limitations

The two-year statute of limitations under Texas Civil Practice & Remedies Code Section 16.003 creates urgency if your claim stalls or faces denial. Filing a lawsuit before the deadline becomes necessary to preserve your rights, which requires immediate attorney involvement. This timeline pressure means that waiting months to decide whether you need legal help can cost you the ability to pursue compensation through the courts if the insurer refuses a fair settlement.

Final Thoughts

Austin auto collision claims follow predictable patterns, but that predictability may work in your favor once you understand the system. Insurance companies operate within legal constraints, and recognizing when they cross from standard investigation into bad-faith tactics positions you to demand fair treatment. The steps you take immediately after a collision-photographing the scene, collecting witness information, reporting to police and your insurer-create the foundation for a stronger claim.

Your rights under Texas comparative negligence law protect you even if you’re partially at fault, but only if you avoid early admissions and statements that undermine your position. The two-year statute of limitations creates real urgency; waiting years to address a stalled claim or lowball offer eliminates your ability to pursue compensation through the courts. Initial settlement offers typically fall 20 to 40 percent below fair value, which means accepting the first number almost always costs you money you’re entitled to recover.

Professional legal representation transforms how insurers treat your Austin auto collision claims. When adjusters know you have an attorney, settlement negotiations shift because they understand trial readiness changes the equation. Contact Heaton Injury Law, PLLC to discuss your claim-the consultation is free, and we’ll explain exactly what your case is worth and what steps come next.

The information provided in this blog is for general informational purposes only and does not constitute legal advice. Every case is unique, and laws may vary by jurisdiction. Reading this content does not create an attorney-client relationship. For guidance specific to your situation, please consult with a qualified personal injury attorney licensed in Texas.

Artificial intelligence may have been used to assist in generating some text or images in these articles.