Meredythe | June 1, 2026 | Blog

Rideshare accidents in Austin create unique legal challenges that differ from standard car crashes. Insurance coverage gaps, liability questions, and settlement decisions can overwhelm injured passengers and drivers.

At Heaton Injury Law, PLLC, we help Austin rideshare accident victims understand their options and fight for fair compensation. This guide walks you through insurance coverage, settlement negotiations, and when taking your case to trial makes sense.

Types of Rideshare Accidents and Injury Claims

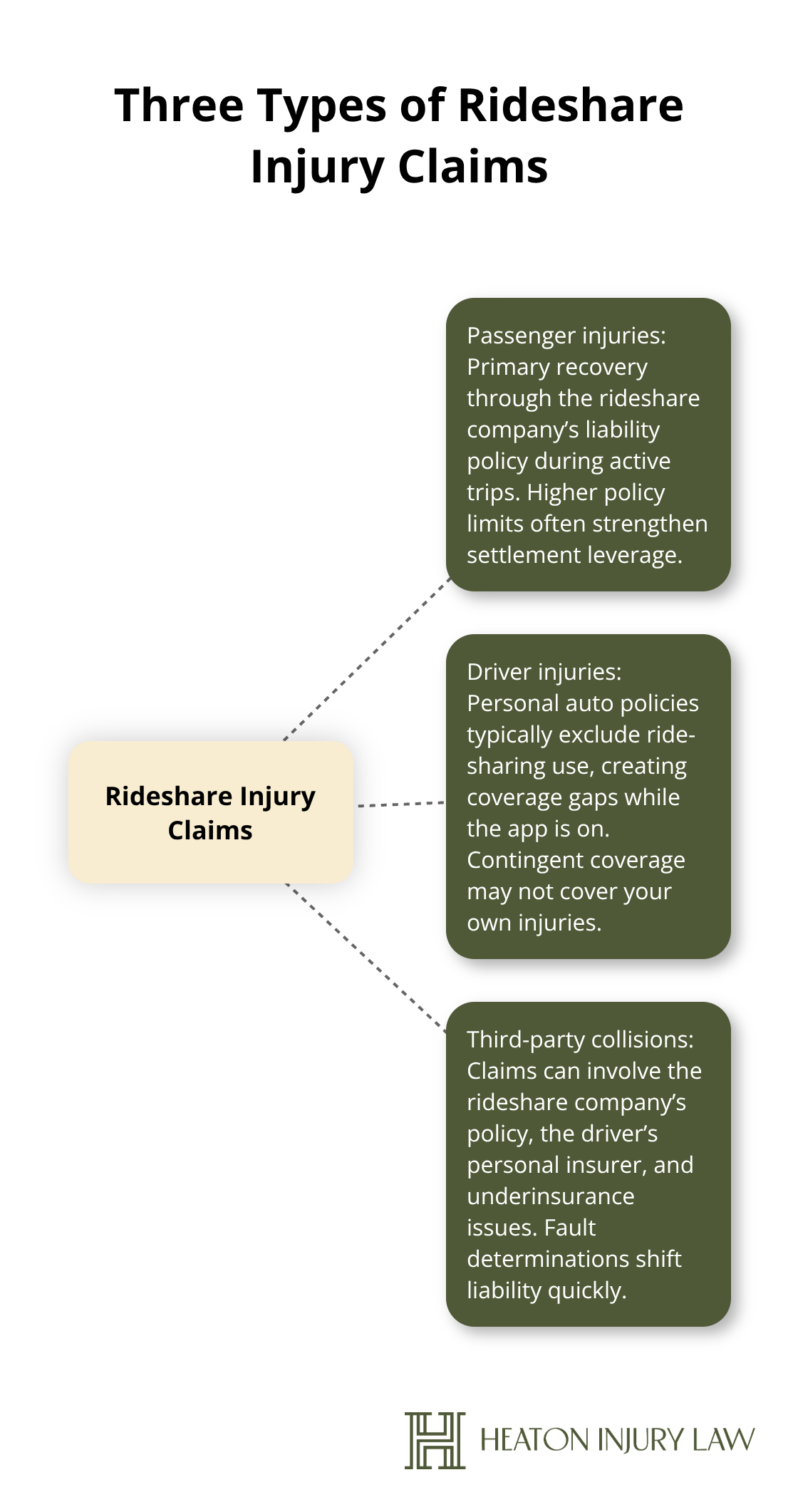

Rideshare accidents in Austin produce three distinct injury patterns, each carrying different liability exposures and insurance complications. Passengers injured during active trips occupy the strongest position because rideshare platforms maintain primary liability coverage when a passenger is aboard. Drivers working for Uber or Lyft encounter murkier liability questions because personal auto policies typically exclude ride-sharing use, leaving coverage gaps during the app-on period before pickup. Third-party collisions-where a rideshare vehicle strikes another driver, pedestrian, or property-create layered claims involving the rideshare company’s insurance, the driver’s personal policy, and potential underinsurance issues.

Passenger Injuries Pack the Strongest Claims

When you suffer injury as a passenger in a rideshare vehicle, the rideshare company’s insurance becomes your primary recovery source. Texas law requires ride-sharing companies to maintain insurance covering injuries to passengers if the driver lacks adequate personal coverage. This means you have a direct claim against the platform’s policy, which carries higher limits than most personal auto policies. The Insurance Research Council reports that accident victims who pursue claims with attorney representation receive settlements approximately 3.5 times higher than those who negotiate alone, making legal guidance essential for passenger claims. You must document your injuries immediately after the accident-seek medical care within 24 to 48 hours and preserve all medical records, as gaps in treatment weaken your claim value. Collect the driver’s name, the rideshare company involved, and passenger contact information from other riders if present. Request the trip details from the app, which establishes the exact moment coverage activated. Photograph your injuries, the vehicle interior, and any visible damage. Many passengers hesitate to report injuries until days later, but insurance adjusters scrutinize delayed reporting as a sign of minimal harm.

Driver Injuries Create Coverage Headaches

Rideshare drivers face a coverage nightmare that personal auto policies rarely address. Most standard policies explicitly exclude commercial use, meaning your personal insurance won’t cover injuries you sustain while the app is active or you transport passengers. The rideshare company provides contingent coverage, but it typically covers only liability you cause to others-not injuries to yourself or your vehicle. This gap leaves drivers severely underprotected. If another driver causes the accident, you can pursue their liability insurance, but if you bear partial fault or the other driver lacks insurance, your recovery shrinks dramatically. Texas law requires drivers to carry uninsured or underinsured motorist coverage, which can bridge gaps when the at-fault party lacks adequate insurance. You should review your UM/UIM limits with an attorney before settling any claim, as these provisions often provide hidden recovery sources.

Third-Party Collisions Demand Immediate Action

Third-party collisions involving rideshare vehicles demand immediate police reports and detailed scene documentation because liability shifts rapidly depending on fault determination. You must photograph all vehicle damage, road conditions, traffic signals, and sight lines. Obtain written statements from passengers and any independent witnesses. The rideshare company will investigate, but their investigation prioritizes their liability exposure, not your recovery. Understanding how insurance coverage applies to your specific accident type determines whether you settle quickly or pursue a trial-a decision that hinges on the strength of your claim and the insurer’s initial offer.

Understanding Insurance Coverage in Rideshare Accidents

Rideshare insurance coverage operates in three distinct layers, and most Austin drivers and passengers misunderstand which layer applies to their accident. The rideshare platform provides primary liability coverage during active trips, but this protection has strict activation windows and significant coverage gaps that catch victims off-guard. Uber and Lyft maintain policies with liability limits typically ranging from $1 million to $1.5 million per incident when a passenger is aboard, but these policies cover only injuries caused to third parties-not damage to the vehicle or injuries to the driver themselves.

The Coverage Gap That Catches Drivers Off-Guard

Your personal auto insurance almost certainly excludes ride-sharing activities, creating a dangerous coverage void during the period when your app is active but you haven’t picked up a passenger yet. The Texas Department of Insurance reports that most personal auto policies explicitly deny coverage for commercial use, and ride-sharing falls squarely into that category. If you suffer injury while driving for Uber or Lyft before your first pickup, you’re technically uninsured unless you purchase a separate ride-sharing policy. Many drivers never discover this gap until they file a claim and face rejection.

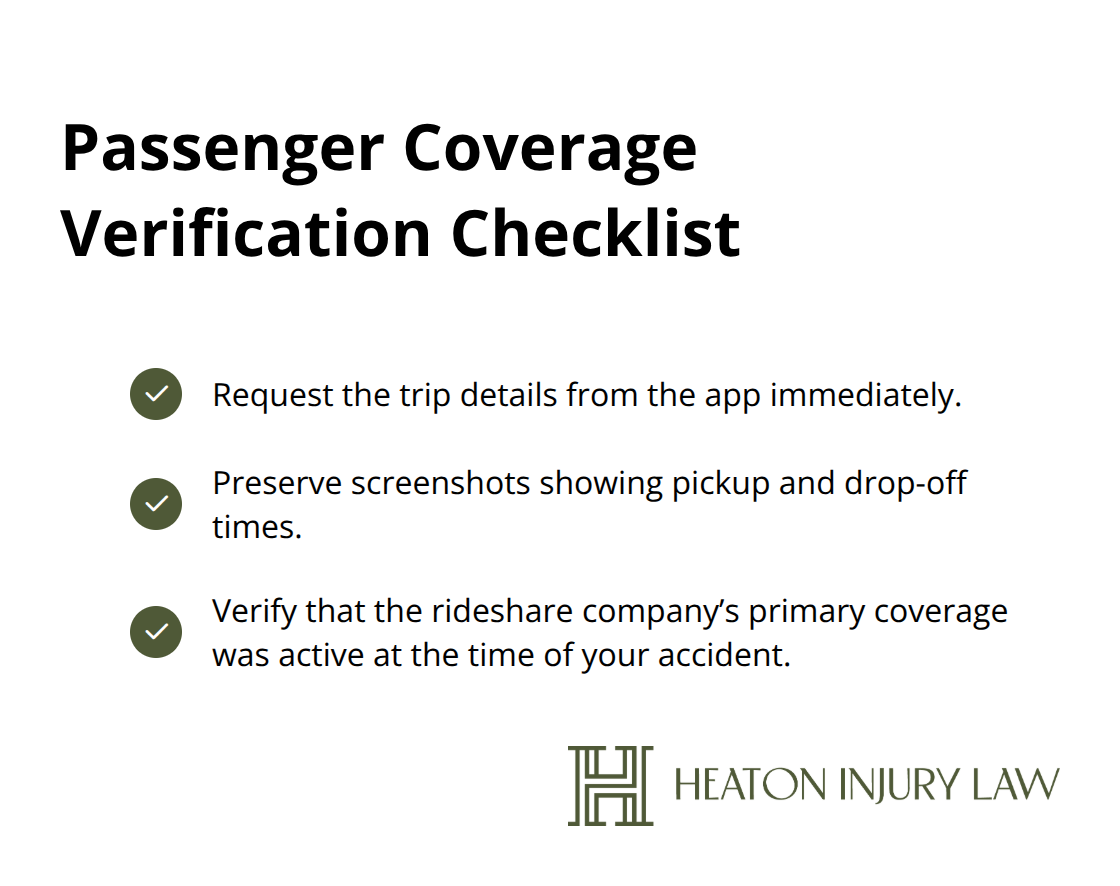

Insurance companies weaponize these gaps aggressively-they’ll deny your claim, cite the policy exclusion, and force you to pursue recovery against the rideshare platform’s contingent coverage, which carries lower limits and stricter conditions. As a passenger, your situation differs significantly because the rideshare company’s primary coverage activates the moment you enter the vehicle, but you must verify this protection existed at the time of your accident. Request the trip details from the app immediately and preserve screenshots showing the exact pickup and drop-off times, as these timestamps prove when coverage was active.

How Adjusters Minimize Your Payout

Insurance adjusters handling rideshare claims operate from a playbook designed to minimize payouts, and they’ll exploit every ambiguity about coverage activation and policy limits to their advantage. They’ll contact you within days, express sympathy, and present a lowball settlement figure that accounts only for immediate medical expenses-never future treatment, lost wages, or pain and suffering. The Insurance Research Council found that accident victims with attorney representation receive approximately 3.5 times higher settlements than those negotiating alone, yet most injured parties attempt to handle claims independently.

Never provide a recorded statement to an adjuster before consulting with an attorney, as these statements become permanent evidence that insurers use to challenge your damages later. When you review any settlement offer, verify exactly which insurance policy covers your claim-the rideshare platform’s policy, the driver’s personal policy, or potentially both-because coverage limits determine your maximum recovery.

Uncovering Hidden Recovery Sources

If the driver carried uninsured or underinsured motorist coverage, that policy can supplement recovery when the at-fault party lacks adequate protection. Collect all policy documents from both the rideshare company and the driver’s personal insurer, document every medical expense immediately, and preserve evidence of lost income before any settlement discussion occurs. Understanding how these coverage layers interact with your specific accident determines whether you settle quickly or pursue a trial-a decision that hinges on the strength of your claim and the insurer’s initial offer.

Settlement or Trial: Which Path Maximizes Your Recovery

Insurance adjusters count on your exhaustion and financial desperation to push you toward quick settlements that undercompensate your injuries. Settlement offers typically arrive within weeks of your accident, and they come with psychological pressure-the adjuster frames the number as final, warns that rejecting it means months of litigation, and suggests that trial outcomes are unpredictable. The Insurance Research Council reports that accident victims who hire an attorney and proceed to trial receive settlements approximately 3.5 times higher than those who accept early offers without representation. This gap exists because trial-ready cases command respect from insurers; they know that an attorney willing to litigate poses genuine risk to their bottom line.

How Settlement Negotiations Work in Rideshare Cases

Settlement negotiations in rideshare cases usually begin when your attorney submits a demand letter that itemizes medical expenses, lost wages, vehicle damage, and pain and suffering. Insurers respond with lowball counteroffers, negotiations stretch across weeks or months, and most cases resolve before trial. However, accepting a settlement means surrendering your right to future compensation-if your injuries worsen or require additional surgery months later, you cannot reopen the claim or seek additional damages. The trade-off is certainty; you know exactly what you receive, avoiding the trial gamble where a jury might award less than your settlement offer or reject your claim entirely.

When Trial Makes Financial Sense

Trial makes financial sense when the insurer’s settlement offer falls significantly below your documented damages or when liability is clear and the jury pool in your Austin district typically favors injured plaintiffs. Trial cases consume 12 to 24 months before verdict, and appeals can extend timelines by two additional years, but the potential for punitive damages in cases involving egregious negligence can dramatically exceed settlement values. Your attorney’s experience with Austin juries, local court procedures, and the specific district judges assigned to your case determines trial viability-a local attorney familiar with jury composition and verdicts in your courthouse provides enormous strategic advantage.

Understanding Fee Arrangements and Cost Recovery

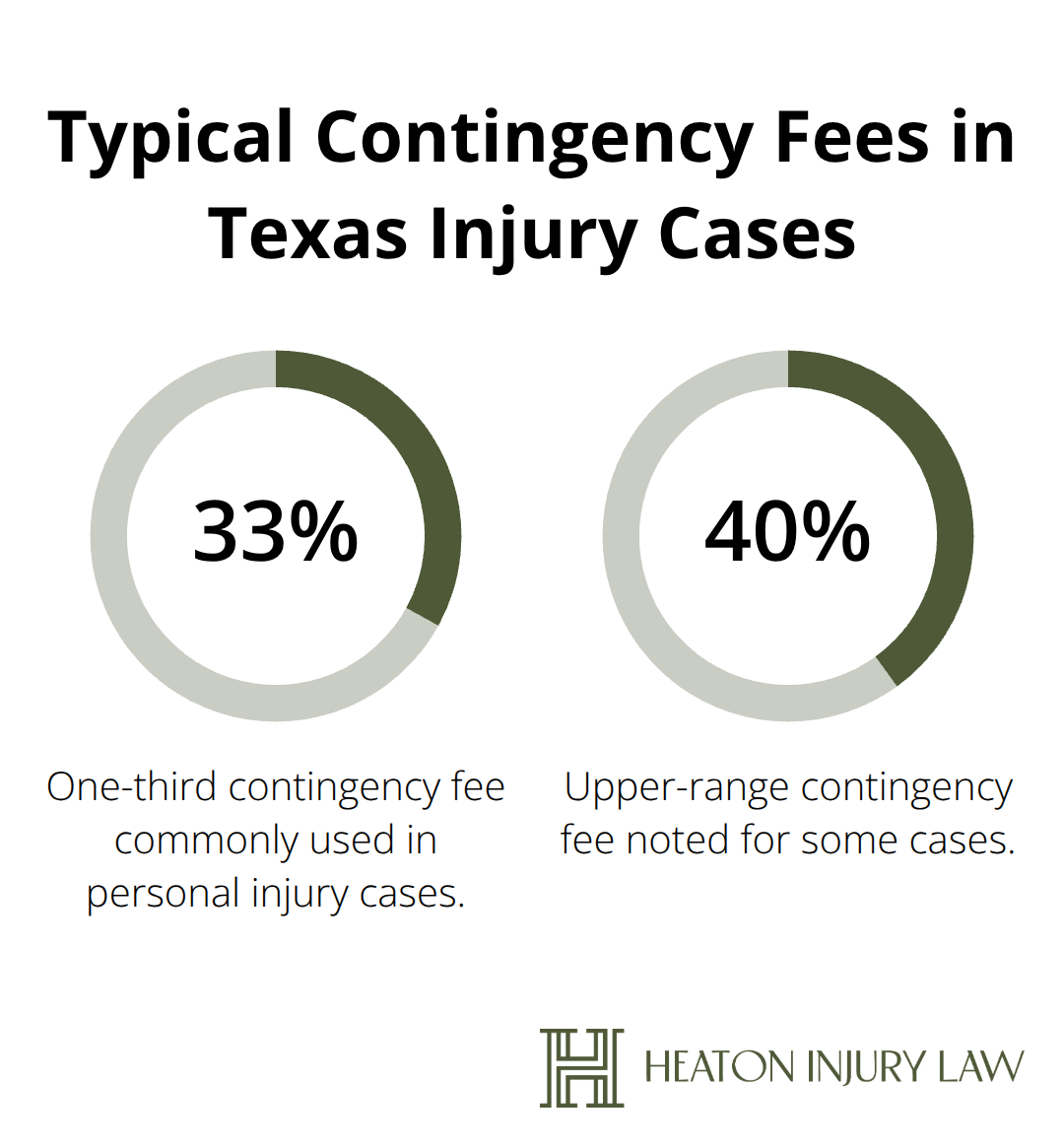

Contingency-fee arrangements, typically ranging from one-third to 40 percent of your recovery, align your attorney’s financial interests with maximizing your payout, whether through settlement or a jury verdict. Medical liens from providers or subrogation claims from health insurers will reduce your net recovery in both scenarios, but your attorney negotiates these liens aggressively to protect your final compensation. The decision between settlement and trial depends on the strength of liability evidence, the defendant’s insurance limits, your medical prognosis, and whether you prioritize certainty over potential higher recovery-factors that require careful analysis with an attorney who understands rideshare liability specifics and Texas personal injury law.

Final Thoughts

Rideshare accidents in Austin demand immediate action and strategic decision-making that most injured victims mishandle without guidance. The insurance coverage landscape shifts based on your role-passenger, driver, or third-party victim-and misunderstanding which policy applies costs you thousands in lost recovery. Settlement offers arrive quickly and feel final, but accepting them prematurely locks you into compensation that rarely accounts for future medical costs or long-term pain and suffering.

Your recovery hinges on three critical decisions: you must document injuries immediately after the accident, refuse to provide recorded statements before consulting an attorney, and evaluate settlement offers against your actual damages rather than accepting the first number an adjuster presents. The Insurance Research Council confirms that accident victims with attorney representation receive approximately 3.5 times higher compensation than those negotiating alone, yet most injured parties attempt claims independently and settle for fractions of what they deserve.

At Heaton Injury Law, PLLC, we understand rideshare liability and help Austin rideshare accident attorney clients navigate settlement and trial decisions with confidence. Contact us for a free consultation to discuss your rideshare accident claim and learn whether settlement or trial serves your financial interests best.

The information provided in this blog is for general informational purposes only and does not constitute legal advice. Every case is unique, and laws may vary by jurisdiction. Reading this content does not create an attorney-client relationship. For guidance specific to your situation, please consult with a qualified personal injury attorney licensed in Texas.

Artificial intelligence may have been used to assist in generating some text or images in these articles.