Meredythe | May 21, 2026 | Blog

A catastrophic injury changes everything-your body, your finances, your future. The medical bills alone can reach hundreds of thousands of dollars, and that’s before accounting for years of ongoing care and lost income.

At Heaton Injury Law, PLLC, we help injured Texans secure the long-term benefits they deserve. As an Austin catastrophic injury attorney, we know how to calculate lifetime care costs and fight insurers who undervalue your claim.

What Counts as a Catastrophic Injury in Texas

Texas law doesn’t use the term catastrophic injury in a single definition. Instead, courts and insurers recognize serious bodily injuries with lasting damage, extreme pain, or life-threatening consequences. Spinal cord injuries resulting in paralysis, traumatic brain injuries affecting memory or cognition, amputations, severe burns covering significant body surface area, crush injuries, and substantial vision or hearing loss all qualify. The distinction matters because catastrophic injuries demand lifetime care planning, not just short-term treatment.

Medical Documentation Establishes Your Claim’s Foundation

Medical documentation becomes your foundation here. Your medical records must show the severity through imaging results, specialist diagnoses, functional capacity evaluations, and rehabilitation assessments. A neurologist’s report on cognitive deficits carries weight. An orthopedic surgeon’s documentation of permanent disability carries weight. Hospital discharge summaries detailing your condition at each stage carry weight.

Without detailed medical evidence, insurers will argue your injury doesn’t warrant long-term benefits and will lowball settlement offers accordingly.

The Financial Reality of Lifetime Care

The true cost of catastrophic injury extends far beyond emergency room visits. A person with a spinal cord injury requiring full-time care faces millions in lifetime expenses depending on age at injury and care setting. A severe traumatic brain injury survivor needing ongoing cognitive rehabilitation, medication management, and supervised living arrangements often requires hundreds of thousand to tens of millions over their lifetime depending on age at the time of injury. These figures come from life-care planning data compiled by medical economists and rehabilitation specialists.

Your lost earning capacity compounds the damage. If you earned $60,000 annually and a catastrophic injury ended your career at age 35, you lost roughly $1.2 million in wages over a typical working life (before accounting for inflation and benefits). Insurance companies know these numbers. They also know most injured people lack the expertise to calculate them accurately. This gap between initial settlement offers and actual lifetime needs becomes dangerous.

Life-Care Plans Drive Claim Valuation

Life-care planners work with physicians, nurses, and rehabilitation specialists to project your specific future care needs. They estimate how many hours of in-home nursing care you’ll need monthly, what assistive devices you’ll require, which medications will cost how much over time, and what facility-level care might become necessary as you age. A life-care plan isn’t theoretical. It’s itemized, priced, and defensible.

Insurers take life-care plans seriously because juries do. When your case reaches trial, a credible life-care plan backed by expert medical testimony shifts the entire valuation of your claim upward by hundreds of thousands or even millions of dollars. Getting expert involvement before settlement discussions begin strengthens your negotiating position considerably. This early coordination with medical professionals and economists transforms how insurers evaluate your claim and what they’re willing to offer.

Navigating Long-Term Care Benefits After a Catastrophic Injury

Medicaid, Medicare, and the Funding Gap You Must Understand

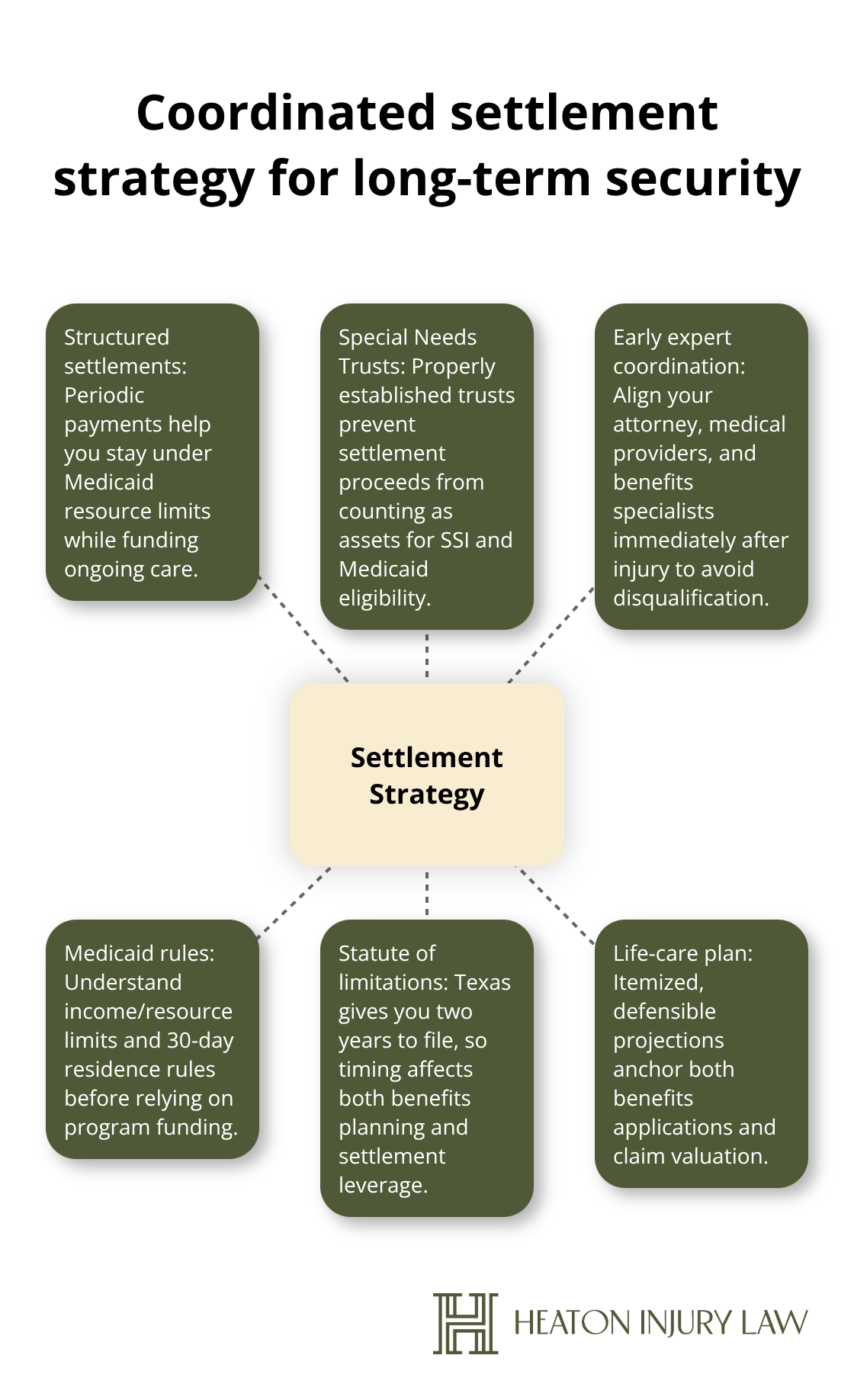

Texas offers multiple pathways to long-term care funding after a catastrophic injury, but the programs operate under strict eligibility rules and tight deadlines that most injured people don’t understand until it’s too late. Medicaid covers the largest share of long-term care costs in Texas, but you must meet income and asset limits that vary depending on whether you apply for home-based services, assisted living, or nursing home care. The critical threshold: your countable resources cannot exceed approximately $2,000 for an individual, though a personal injury settlement paid as a lump sum will likely immediately disqualify you from Medicaid eligibility in the month you receive it and potentially for years afterward unless you structure the settlement strategically. Medicare, despite covering some acute medical care, does not pay for long-term care services-a gap that catches most people off guard. You must apply through Your Texas Benefits portal, and you typically cannot access Medicaid-funded nursing home services until you’ve resided there for 30 consecutive days, meaning you’ll need alternative funding sources initially.

The Two-Year Clock That Controls Everything

The statute of limitations for filing your personal injury claim is two years from the date of injury under Texas Civil Practice & Remedies Code Section 16.003, so delay in pursuing your claim directly impacts both your settlement timeline and your ability to fund ongoing care while waiting for recovery. This deadline creates urgency that extends beyond the courtroom-it affects your benefits planning, your medical documentation timeline, and your ability to coordinate with specialists who will establish your care needs.

Medical Documentation Determines Your Benefit Approval

Working with medical experts early transforms how benefits agencies evaluate your case and what funding they approve. Your physician must document not just your diagnosis but your functional limitations in writing-how many hours of assistance you need daily, what tasks you cannot perform independently, whether you require skilled nursing versus personal care assistance. This distinction determines whether you qualify for Medicaid, what type of facility or home care the state will fund, and how much monthly benefit you receive. Life-care planners, working alongside your medical team, create itemized projections of your future care costs that become the foundation for both benefit applications and settlement negotiations.

Structured Settlements Preserve Your Medicaid Eligibility

Structured settlements-spreading lump-sum payments over time rather than receiving everything at once-have grown significantly as a strategy, with 2023 premiums reaching approximately $8.6 billion, because periodic payments allow you to stay under Medicaid’s resource limits while preserving long-term care coverage. Special Needs Trusts shield settlement proceeds from counting as assets for SSI and Medicaid eligibility, but you must establish them before funds are disbursed, not after. Starting this coordination between your attorney, medical providers, and benefits specialists immediately after your injury-not months into your case-prevents the catastrophic mistake of accepting a settlement structured wrong and losing Medicaid coverage that you desperately need for ongoing care.

Timing Your Settlement Structure Determines Your Long-Term Security

The coordination between your personal injury recovery and your benefits eligibility cannot happen after settlement arrives. Medical experts must establish your care needs now. Your attorney must understand how settlement structure affects your Medicaid qualification. Your benefits specialist must know what asset limits apply to your specific situation.

This multidisciplinary approach, started early, transforms a settlement from a single lump payment into a comprehensive funding strategy that protects both your immediate recovery and your decades of future care. When these elements align before settlement discussions begin, your negotiating position strengthens considerably, and insurers recognize that you’ve prepared for the full scope of your lifetime needs.

How We Maximize Your Recovery

Insurance companies calculate catastrophic injury claims using formulas designed to minimize what they pay you. We calculate them using the actual cost of your lifetime care, which produces dramatically different numbers. The gap between these two approaches determines whether you accept an offer that funds five years of care or one that funds fifty years.

Establishing Your Medical Foundation

We start by establishing your baseline medical facts through detailed physician reports, functional capacity evaluations, and specialist assessments that quantify exactly what your body can and cannot do. A life-care planner then projects your specific future needs-not generic estimates, but itemized costs for in-home nursing hours, assistive equipment, medications, facility care, and home modifications based on your age, injury type, and local Austin market rates. When a spinal cord injury survivor needs full-time care, that projection might span sixty years and total $3.2 million rather than the $800,000 an insurer initially offers.

Accounting for Real-World Cost Growth

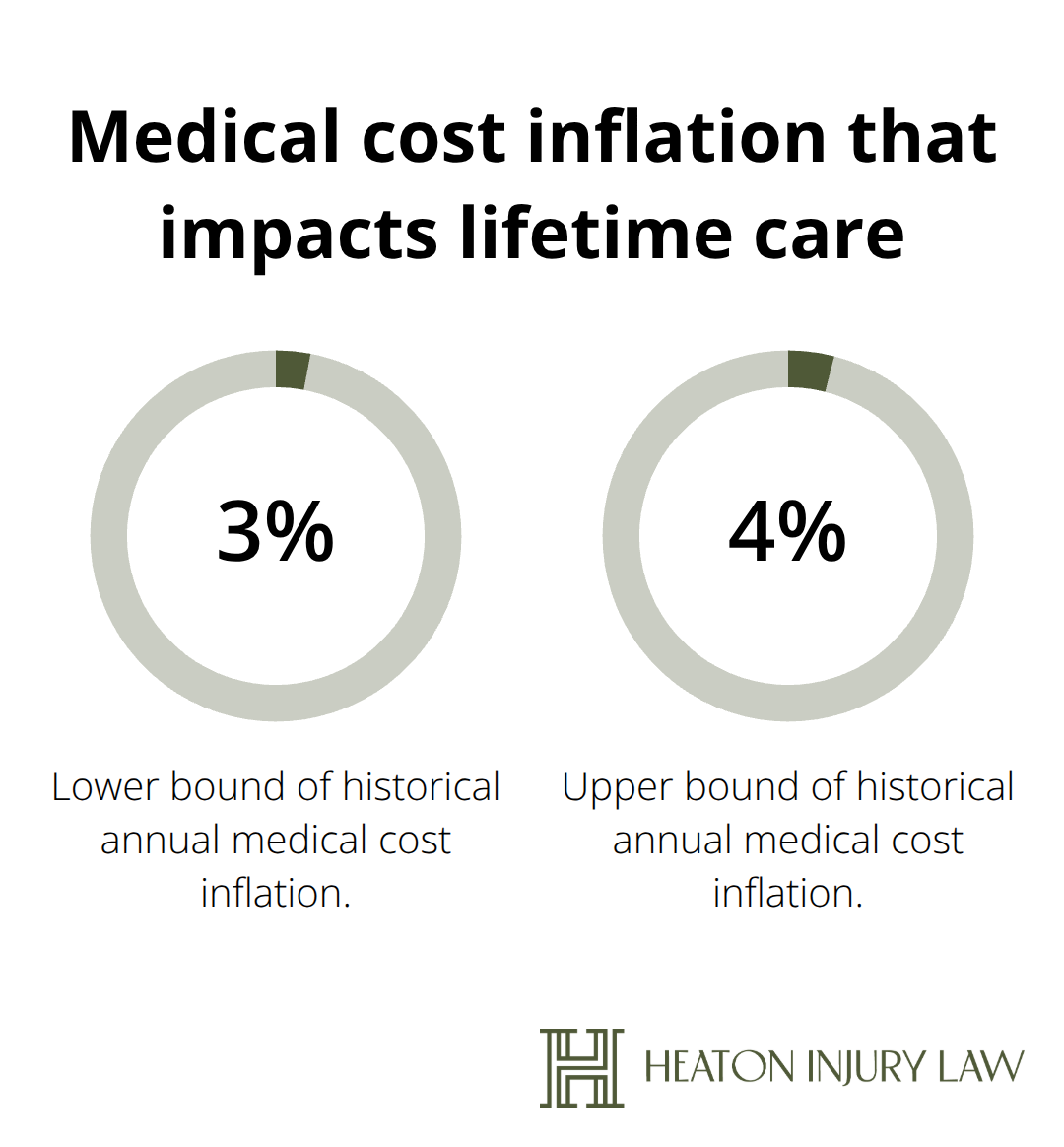

The difference comes from accounting for inflation in medical costs, which historically averages 3 to 4 percent annually according to healthcare economic data, compound growth in your care needs as you age, and the actual hourly rates paid to qualified caregivers in the Austin area rather than national minimums. We coordinate with medical economists who testify about lost earning capacity, vocational experts who document your inability to return to work, and rehabilitation specialists who establish why your care needs will increase over time rather than decrease. This expert foundation transforms settlement negotiations because insurers know that if your case reaches trial, a jury will hear from credible professionals backing every dollar of your claim.

Shifting the Power in Negotiations

Negotiating from this position eliminates the power imbalance that favors insurance companies in most injury cases. We present settlement demands backed by itemized life-care plans, medical testimony, and economic analysis that insurers cannot easily dismiss as inflated or speculative. When insurers recognize that we’ve prepared for trial and that a jury would likely award substantially more than their current offer, settlement discussions shift dramatically. Insurers take structured settlement discussions seriously once they understand you’ve coordinated with benefits specialists to preserve Medicaid eligibility through periodic payments rather than lump sums, because this demonstrates sophistication about long-term funding that extends beyond a single settlement check.

Preparing for Trial When Necessary

If settlement offers remain inadequate despite this preparation, we proceed to trial with every expert, every medical record, and every damage calculation ready for presentation. Trial preparation for catastrophic injury cases requires months of work-depositions of treating physicians, cross-examination strategies for defense experts, jury presentation materials that make lifetime care costs tangible rather than abstract. Most cases settle before trial because insurers understand the risk, but we treat every case as trial-ready from the beginning, which fundamentally changes how seriously they approach negotiations with us.

Final Thoughts

A catastrophic injury in Texas demands more than emergency medical care-it demands a strategy that accounts for decades of future expenses, protects your eligibility for long-term care benefits, and secures compensation that actually covers what your lifetime recovery will cost. The gap between what insurance companies initially offer and what your care truly requires often reaches hundreds of thousands of dollars, and that gap exists because most injured people negotiate alone without the medical expertise, benefits knowledge, or trial preparation that shifts settlement discussions in their favor. Your medical records establish the foundation, your life-care plan quantifies the cost, your structured settlement preserves your Medicaid eligibility, and your attorney’s trial readiness forces insurers to take your claim seriously-these elements work together only when coordinated from the beginning, not assembled after settlement arrives.

An Austin catastrophic injury attorney with experience in lifetime care planning, benefits coordination, and insurer negotiation transforms how your claim is valued and what you ultimately recover. We at Heaton Injury Law, PLLC understand how catastrophic injuries affect your future and how to build claims that reflect that reality. We work on contingency, meaning you pay nothing unless we win.

Contact us for a free consultation to review your claim, discuss your care needs, and develop a strategy that protects your future.

The information provided in this blog is for general informational purposes only and does not constitute legal advice. Every case is unique, and laws may vary by jurisdiction. Reading this content does not create an attorney-client relationship. For guidance specific to your situation, please consult with a qualified personal injury attorney licensed in Texas.

Artificial intelligence may have been used to assist in generating some text or images in these articles.