Meredythe | May 26, 2026 | Blog

Car crashes happen fast, but the legal aftermath moves slowly. Texas liability laws work differently than most states, which means your recovery depends on understanding how fault is determined here.

At Heaton Injury Law, PLLC, we help injured Texans navigate these rules and protect their rights. The steps you take immediately after a crash can make or break your case.

How Texas Fault Rules Reduce Your Recovery

Texas applies a modified comparative negligence rule, which fundamentally changes how much compensation you can receive. Under Texas Civil Practice & Remedies Code §33.001, you can only recover damages if you are less than 50% at fault for the crash. This is not a minor technicality-it directly impacts your settlement amount. If you are found to be 30% at fault, your total recovery is reduced by exactly 30%. If you reach 50% or higher, you recover nothing. This rule exists in Texas and many other states, but it differs sharply from pure comparative negligence states like California, where you can recover even if you are 99% at fault (though your award is reduced accordingly). The difference matters significantly when liability is contested or when your actions contributed partially to the crash.

Why Texas’s Rule Creates Immediate Pressure on Evidence

The 50% threshold creates intense pressure to establish fault quickly and thoroughly. Insurance adjusters know this rule and will aggressively argue that you bear some responsibility to reduce their payout. Distracted driving, speeding, or even minor traffic violations on your part can be weaponized to claim comparative fault. A rear-end collision appears straightforward, but if you were speeding or had a broken taillight, the other driver’s insurer will claim you contributed to the accident. You must photograph the scene immediately-road conditions, traffic signals, vehicle damage patterns, and witness statements all support your position before anyone disputes liability. Police reports from the scene carry significant weight, which is why you should call 911 after any injury crash. The Texas Department of Transportation data shows that roughly a quarter to nearly a third of Texas crashes involve impaired driving, distracted driving accounts for roughly a fifth to a quarter of crashes, and failure to yield remains a leading cause. Understanding which category your crash falls into helps frame the liability narrative in your favor.

How Insurance Companies Exploit the 50% Rule

Insurance companies exploit the comparative negligence rule to pressure injured people into accepting lower offers. They present exaggerated versions of your role in the crash and claim you were 40%, 35%, or even 50% at fault to justify paying less. Once they plant doubt about your fault percentage, many injured people accept reduced settlements rather than risk a trial where a jury might agree. You must establish your fault percentage below 50% with solid evidence and clear documentation. Medical records, wage loss documentation, repair estimates, and expert reconstruction analysis all strengthen your position by focusing attention on the other driver’s conduct rather than yours. If you delay seeking legal guidance, you lose the advantage of early evidence collection and expert analysis. The longer you wait, the more difficult it becomes to counter the insurance company’s narrative about your supposed role in the crash.

What Happens When Liability Becomes Contested

Contested liability cases demand more than photographs and police reports. Insurance adjusters will scrutinize your actions at the time of the crash, looking for any behavior that supports their comparative fault argument. They examine traffic camera footage, dashcam recordings, witness statements, and even your social media posts to build a narrative that you contributed to the accident. You need expert witnesses-accident reconstructionists, engineers, and medical professionals-to counter these claims with objective analysis. These experts examine vehicle damage patterns, road conditions, sight lines, and physics to establish what actually happened. The cost of expert testimony rises quickly, but without it, you face a significant disadvantage against well-funded insurance companies. The evidence you preserve at the scene becomes the foundation for expert analysis later, which is why immediate action matters so much.

Building Your Case Before Settlement Talks Begin

Settlement negotiations begin the moment you file a claim, not when you sit down at a table. Insurance adjusters assess your case strength based on the evidence you present in your initial demand package. A comprehensive package includes the police report, medical records, photographs from the scene, repair estimates, wage loss documentation, and witness statements. You strengthen your position by showing the adjuster that you have thoroughly documented the crash and that liability clearly rests with the other driver. Weak evidence invites aggressive counterclaims about your fault; strong evidence forces the insurer to acknowledge their driver’s responsibility. The comparative negligence rule means that every percentage point matters-the difference between being found 20% at fault and 40% at fault could mean tens of thousands of dollars in your pocket. This is why the evidence you collect in the first hours after the crash shapes your entire recovery.

What Causes Most Texas Crashes and How Liability Gets Determined

Distracted Driving and the Comparative Negligence Trap

Distracted driving accounts for roughly a fifth to a quarter of all Texas crashes, yet insurance companies routinely downplay its significance when their insured driver caused the accident. The moment you mention that the other driver was texting, eating, or adjusting their GPS, adjusters claim your own momentary inattention contributed equally to the collision. This is where the comparative negligence rule becomes a weapon against you. Texas Department of Transportation data shows that impaired driving causes roughly a quarter to nearly a third of crashes, followed by failure to yield as another major category. Speed compounds the problem significantly-crashes at higher speeds produce catastrophic injuries and damage patterns that clearly show the at-fault driver’s recklessness. When speed is involved, liability becomes harder to contest because physics and vehicle damage tell an objective story.

Weather Conditions and Shared Responsibility Arguments

Weather-related accidents present a different challenge. Rain, fog, and ice reduce visibility and traction, but they do not eliminate the duty to drive safely. Insurance companies exploit weather conditions to argue that both drivers shared responsibility because neither could control the elements. This argument fails when you can prove the other driver was speeding, following too closely, or failed to adjust their speed for conditions. Document road conditions, visibility, and weather at the scene with photographs and video. Police reports typically note weather conditions, which creates official documentation that supports your claim.

Commercial Vehicle Violations and Multiple Liable Parties

Commercial vehicle and truck collisions demand specialized liability analysis because federal regulations govern how truck drivers operate. The Federal Motor Carrier Safety Administration sets hours-of-service rules, maintenance standards, and weight limits that trucks must follow. When a truck driver violates these regulations and causes a crash, liability becomes clear-cut because the violation itself may establish negligence. Truck companies also face vicarious liability for their drivers’ conduct, meaning you can pursue compensation directly from the company rather than relying solely on the driver’s insurance. Truck crashes often involve multiple negligent parties-the driver, the trucking company, the maintenance contractor, the cargo loader, or the manufacturer if a mechanical failure contributed. This multiplicity of potential defendants actually strengthens your position because you can pursue recovery from whoever has adequate insurance coverage. The key to liability determination in any crash category is assembling objective evidence immediately.

Building Your Evidence Package for Maximum Impact

Photographs showing skid marks, vehicle positions, and damage patterns speak louder than either driver’s account of what happened. Witness statements from neutral parties carry significant weight because they lack motivation to favor either side. Police reports create official documentation that adjusters cannot easily dismiss. Medical records establish that you suffered genuine injury, which connects the crash directly to your damages. The stronger your evidence package, the harder it becomes for insurance companies to argue comparative fault, and the higher your settlement leverage becomes. These initial steps you take at the crash scene directly influence how adjusters evaluate your claim and what settlement offers they present.

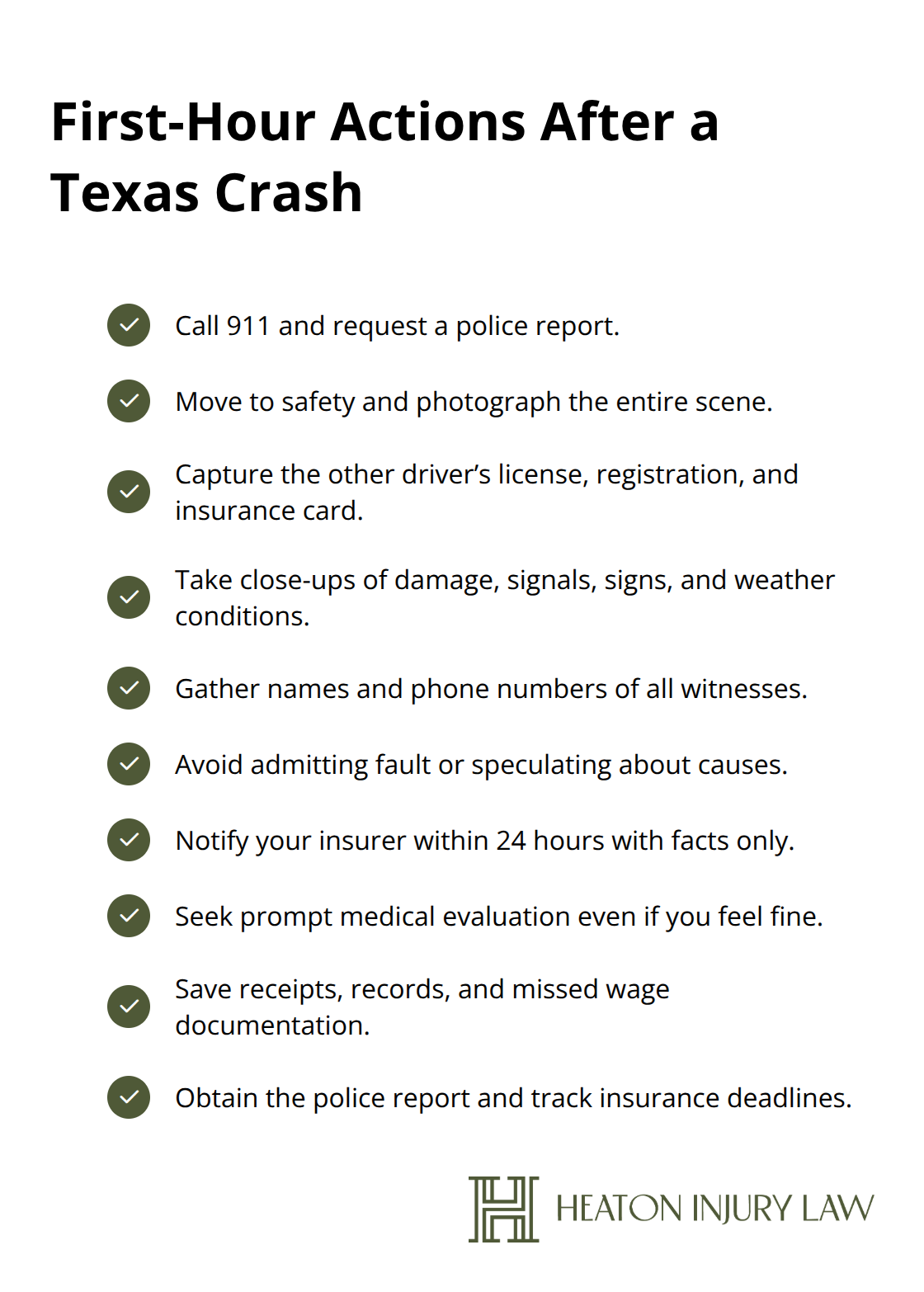

What to Do Immediately After a Crash to Protect Your Claim

The first hour after a crash determines whether you win or lose the comparative negligence battle. Insurance adjusters know that people in shock make poor decisions, so they exploit that vulnerability by calling injured drivers within hours and asking leading questions designed to extract admissions of fault. You must move faster than the insurance company and control the narrative before anyone else does.

Call 911 and Document the Scene

Start by calling 911 if anyone is injured or if damage exceeds $1,000-Texas law requires a police report for these situations, and that official documentation becomes your foundation for countering liability disputes later. Once emergency responders arrive, move to safety if possible and use your phone to photograph everything before the scene changes. Take photos of vehicle damage from multiple angles, road conditions, traffic signals, street signs, weather, and the overall scene layout. Photograph the other driver’s license, vehicle registration, and insurance card directly from the documents themselves-do not rely on memory or handwritten notes.

Gather Witness Information and Control Your Statements

Get the names and phone numbers of any witnesses at the scene, even if they seem minor. Insurance companies will later claim witnesses do not exist or cannot be located, so your contemporaneous documentation becomes critical evidence. Do not discuss fault with the other driver, do not apologize, and do not make statements like “I did not see you” or “I was not paying attention.” Stick to factual observations: “I was traveling at the speed limit,” “the traffic light was green,” or “the other vehicle crossed into my lane.” These factual statements do not admit fault; they establish your version of events while the scene is fresh.

Notify Your Insurer and Seek Medical Care

After leaving the scene, notify your insurance company within 24 hours and provide only the facts you documented-do not speculate about fault and do not volunteer information the adjuster does not ask for. Seek medical evaluation immediately, even if you feel fine, because some injuries like whiplash and concussions manifest hours or days later, and Texas courts view delayed medical treatment as suspicious. Keep every receipt from medical visits, pharmacy expenses, and transportation costs because these establish your economic damages. If you miss work, document those missed wages with pay stubs or employer statements showing hours lost.

Track Insurance Deadlines and Obtain the Police Report

The Texas Insurance Code requires insurers to acknowledge your claim within 15 days and make a coverage decision within 15 business days after you provide proof of loss, so track these deadlines carefully. Request a copy of the police report once it is filed-the report number typically appears on your incident documentation, and you can obtain it from the police department or through the Texas Department of Transportation database. Compare the police report against your scene documentation; if the officer made errors about vehicle positions, traffic signals, or fault findings, note these discrepancies because they support your version of events.

Avoid Settlement Before Legal Consultation

Do not settle with the other driver’s insurance company before consulting with an attorney, because once you sign a release, you forfeit all future claims regardless of how your injuries worsen or how your medical costs escalate. At Heaton Injury Law, PLLC, we help injured Texans understand their rights before accepting any settlement offer. The evidence you preserve at the crash scene directly influences how adjusters evaluate your claim and what settlement offers they present.

Final Thoughts

Texas liability laws operate under rules that directly reduce your recovery if you share any fault for the crash. The modified comparative negligence rule means that every percentage point of fault costs you money, and insurance companies exploit this framework aggressively to minimize their payouts. The evidence you gather in the first hours after an accident becomes your strongest defense against comparative fault arguments, and photographs, witness statements, and police reports create an objective record that adjusters cannot easily dispute.

A Texas car crash attorney brings insider knowledge of how insurance companies operate and what evidence carries the most weight in liability disputes. At Heaton Injury Law, PLLC, we understand the tactics adjusters use to shift blame onto injured drivers, and we build cases that counter these strategies with solid documentation and expert analysis. We handle car crashes, motorcycle accidents, truck collisions, and catastrophic injuries across Texas, and we work on contingency so you pay nothing unless we recover compensation for you.

Contact us for a consultation about your crash and let us help you navigate liability rules that protect your rights. The steps you take today determine the outcome of your case.

The information provided in this blog is for general informational purposes only and does not constitute legal advice. Every case is unique, and laws may vary by jurisdiction. Reading this content does not create an attorney-client relationship. For guidance specific to your situation, please consult with a qualified personal injury attorney licensed in Texas.

Artificial intelligence may have been used to assist in generating some text or images in these articles.