Meredythe | April 16, 2026 | Blog

A personal injury settlement in Austin should fully compensate you for medical bills, lost wages, and other damages you’ve suffered. Insurance companies often undervalue claims, which is why understanding how settlements work puts you in a stronger position.

We at Heaton Injury Law, PLLC help injured Austinites navigate this process and fight for fair compensation. This guide walks you through the key factors that determine your settlement amount and how to negotiate effectively.

What Medical Costs Your Settlement Actually Covers

Medical expenses form the backbone of your personal injury settlement in Austin, and insurance companies know this. They scrutinize every bill, every treatment, and every provider visit to find reasons to reduce what you owe. Texas law recognizes a broad range of medical costs as recoverable damages, but only if you document them properly and understand what insurers will and won’t pay.

Immediate and Ongoing Medical Treatment

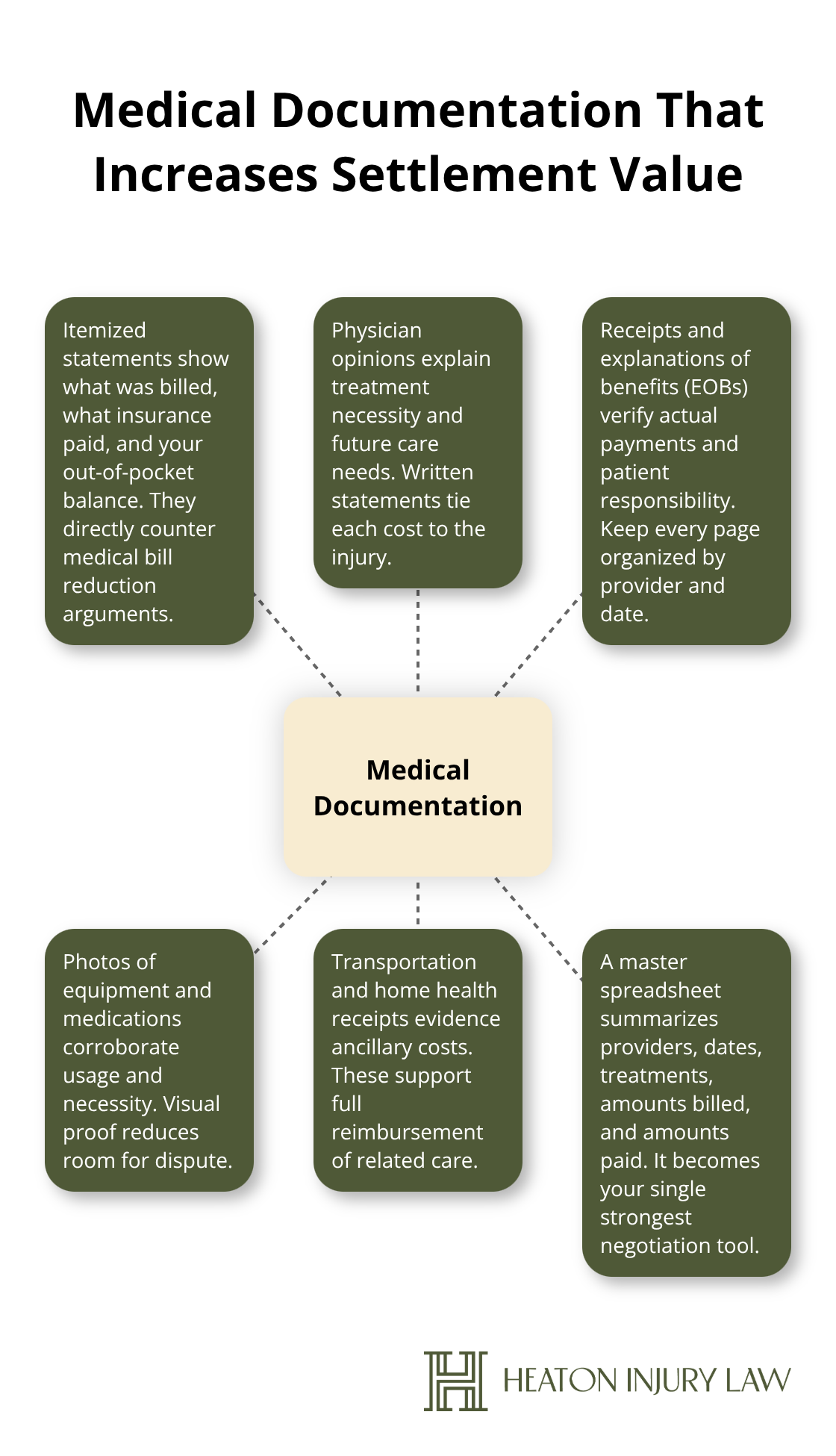

Emergency room visits, hospital stays, surgeries, and imaging related to the collision count as recoverable expenses. Related physical therapy, mental health counseling, and ongoing specialist care qualify too. Prescription medications, medical devices like braces or wheelchairs, and home health care all fall into potentially recoverable categories. The detail most injured people miss is that future medical care belongs in your settlement as well. If your doctor projects you’ll need ongoing physical therapy or future surgery related to your injury, those projected costs should be included now, not later.

Insurance companies fight future medical claims aggressively because they increase your settlement value significantly. You need written opinions from your treating physicians outlining what care you’ll need and for how long. Without this documentation, insurers will claim your injury has fully resolved and deny future medical claims outright. Obtain these opinions in writing before you settle.

Building Your Documentation Arsenal

Medical bills alone won’t maximize your settlement-you need itemized statements showing exactly what was billed, what your insurance paid, and what you owe out of pocket. Keep every receipt, every invoice, and every explanation of benefits letter your insurance company sends. Paycheck stubs showing deductions for medical expenses matter too. Photos of medical equipment, receipts for over-the-counter pain medication and supplies, and receipts from medical transportation count as supporting evidence.

Insurance adjusters use a tactic called medical bill reduction or third party audit companies, where they claim certain treatments weren’t necessary or were overpriced. Organized, detailed documentation lets you push back effectively. Create a spreadsheet listing every medical provider, the dates of service, the type of treatment, the amount billed, and the amount paid. This single document becomes your strongest negotiation tool.

Insurance companies respect organized claimants because they know you’ll fight harder and are less likely to accept lowball offers.

How Insurers Calculate Medical Damages

Insurance companies apply formulas to reduce what they actually pay you. They may claim treatments were excessive, that certain providers charged inflated rates, or that your recovery timeline was longer than necessary. They’ll also argue that some expenses weren’t directly caused by your injury. Understanding their playbook helps you counter their arguments with solid evidence.

Your documentation directly challenges their reduction tactics. When you present organized medical records with physician statements supporting each treatment, insurers lose their ability to dismiss your claims as inflated or unnecessary. The stronger your paper trail, the higher your settlement leverage becomes. This foundation of medical evidence also sets you up to address lost wages and income recovery-the next critical component of your Austin personal injury settlement.

Lost Wages in Your Austin Settlement

Lost wages represent the second pillar of your personal injury settlement, and Texas law classifies them as special damages-meaning you recover the exact amount you lost, not an estimate. This differs fundamentally from how insurance companies evaluate your claim. If you missed work because of your injury, you’re entitled to compensation for the amount you would have earned during that time. The challenge isn’t whether you can recover lost wages; it’s documenting them thoroughly enough that insurers can’t dispute the amount.

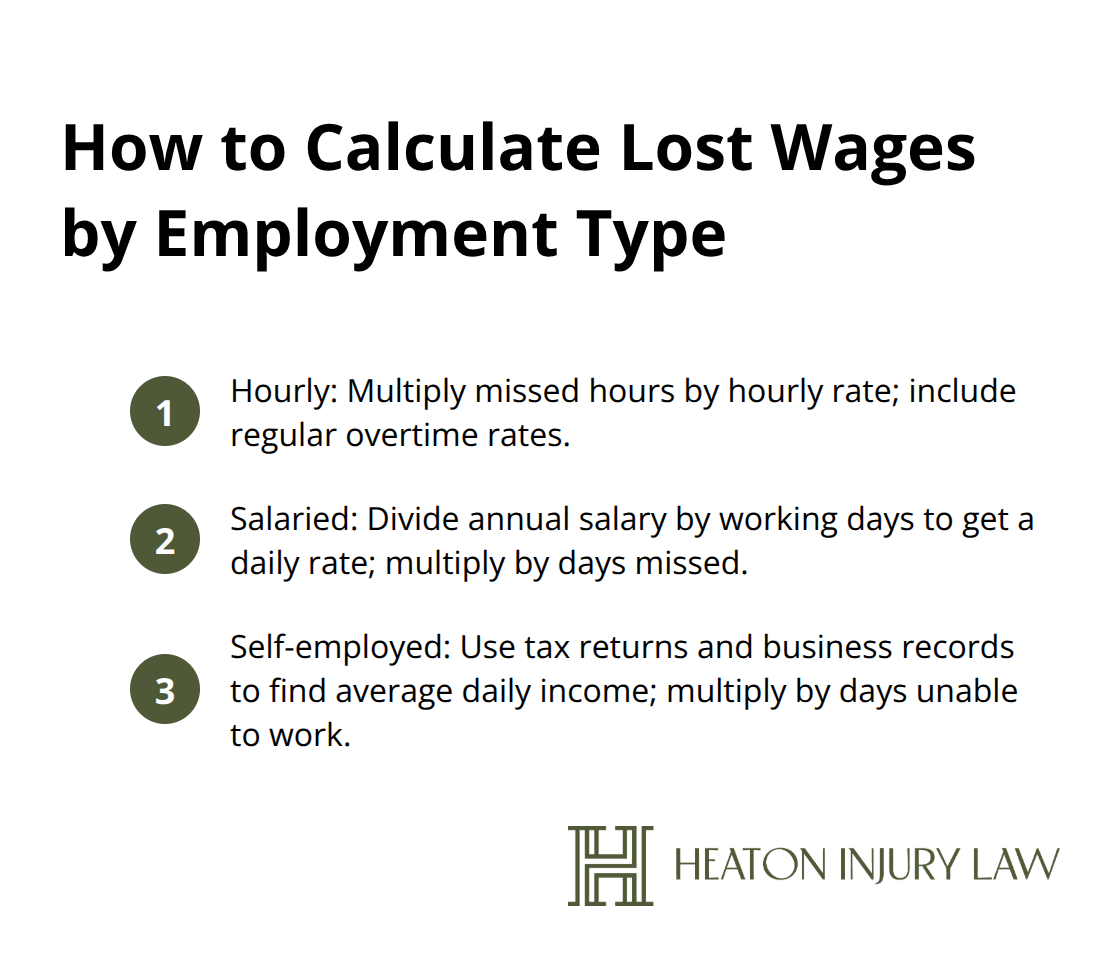

Calculating Lost Wages by Employment Type

Hourly workers multiply missed hours by their hourly rate, accounting for overtime rates if you regularly worked overtime. Salaried employees calculate their average daily wage by dividing annual salary by working days and multiplying by days missed. Self-employed individuals face a tougher road because their income fluctuates, but you can use tax returns and business records to establish an average daily income, then multiply by days unable to work.

Include employment benefits in your calculation-bonuses, vacation days, sick leave, retirement contributions, and health insurance premiums all count as lost wages components. Paycheck stubs, W-2 forms, tax returns, and employer letters confirming days missed become your evidence. Many injured people underestimate this number by forgetting benefits or by failing to account for the full scope of missed work days.

Documentation That Stops Insurer Pushback

Insurance adjusters deliberately lowball lost wage claims because they assume injured people won’t fight back with documentation. Self-employed workers and gig economy participants face even steeper challenges because insurers claim income was uncertain or inconsistent. Push back aggressively with historical financial statements, cancelled contracts you lost due to your injury, and client records showing regular income patterns.

Organize your wage documentation into a single spreadsheet listing employer name, dates of employment, hourly rate or salary, hours or days missed, and total lost wages. This single document transforms your negotiating position. Insurance companies respect organized claimants because they know you’ll fight harder and are less likely to accept lowball offers.

Future Earning Capacity and Long-Term Income Loss

Future earning capacity matters equally-if your injury creates ongoing limitations that reduce your earning potential, Texas courts recognize this as a separate damages category beyond immediate lost wages. A physician’s written statement about your long-term work capacity directly increases the strength of this claim and as a result, your settlement value. For instance, if a back injury prevents you from returning to heavy manual labor, a doctor’s opinion documenting permanent restrictions strengthens your claim for reduced earning capacity damages.

Insurance adjusters systematically undervalue lost wage claims because most injured people lack organized documentation. They count on you settling quickly before you’ve gathered complete financial records. Delaying settlement until you’ve compiled comprehensive wage documentation-including projections for future income loss-positions you for substantially higher recovery amounts. This foundation of wage evidence, combined with your medical documentation, creates the leverage you need when negotiating settlement demands.

How to Respond When Insurers Lowball Your Claim

Anchor Your Demand With Evidence, Not Emotion

Insurance adjusters operate from a predictable playbook: they submit an initial settlement offer far below what your case is worth, hoping you’ll accept out of desperation or exhaustion. In Texas, the median personal injury settlement sits at just $12,281 according to Jury Verdict Research, while the average verdict reaches $826,892-a stark gap that reveals how settlements cluster at the low end unless you push back strategically. Your first response to any lowball offer determines whether you’ll accept pennies on the dollar or fight for actual compensation.

Most injured people make their biggest mistake right here: they treat the insurer’s opening number as a starting point for negotiation rather than recognizing it for what it is-an anchor designed to suppress your expectations. Reject this frame entirely. Your demand letter should anchor high but reasonably, grounded in the medical and wage documentation you’ve compiled. If you’ve documented $50,000 in medical expenses and $30,000 in lost wages, your demand should reflect the full economic damages plus a multiplier for pain and suffering-typically 2 and sometimes up to many multiples of your economic damages depending on injury severity.

Counter With Specific Evidence, Not General Arguments

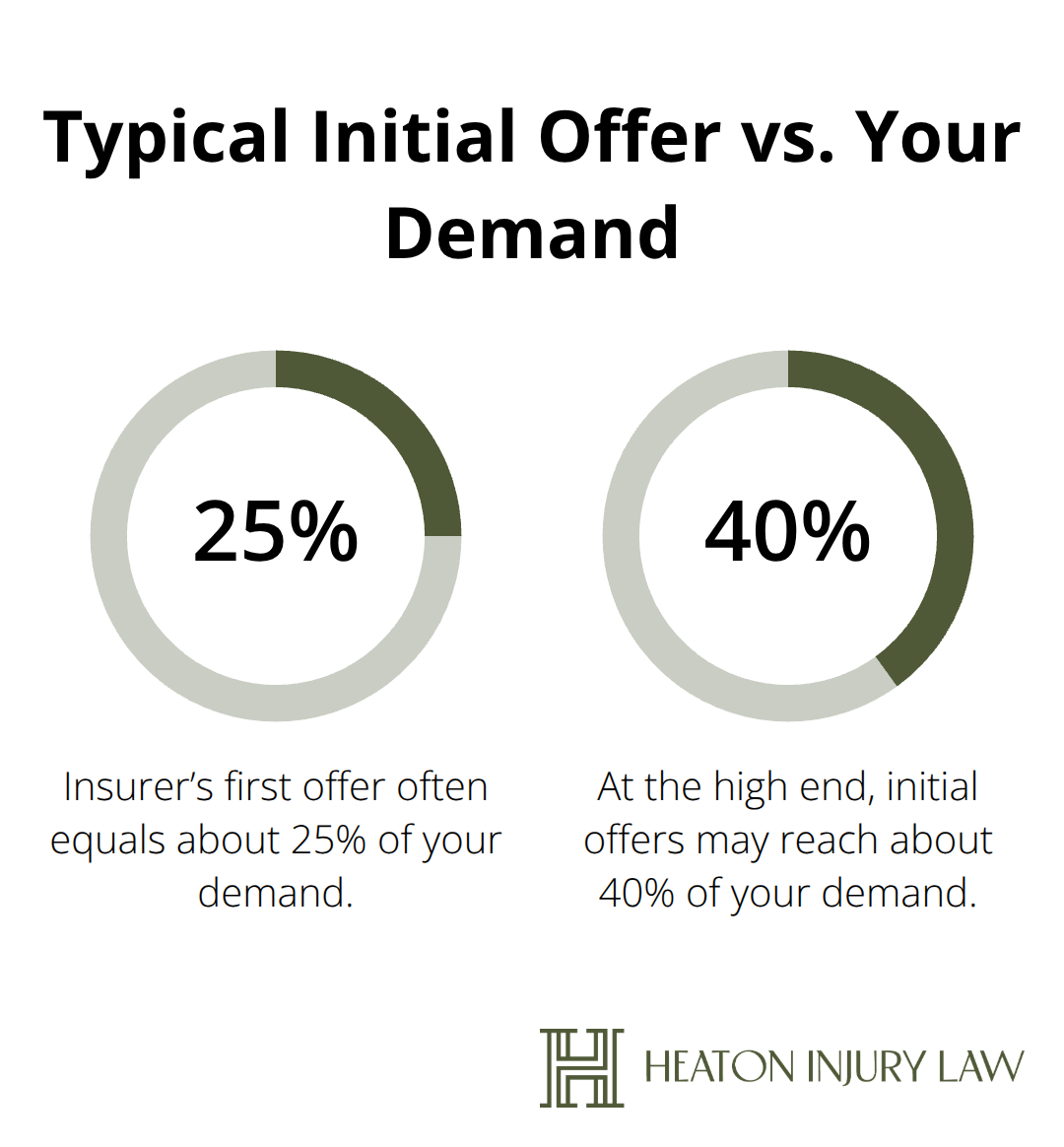

The insurer’s first offer will inevitably fall substantially lower-often 25 to 40 percent of your demand. This isn’t a negotiation; it’s a test to see if you’ll crumble. Counter with a higher demand supported by specific evidence: point to medical provider statements that justify treatment necessity, reference your employer’s confirmation of missed work days, cite your tax returns showing self-employment income, and highlight any gaps in the insurer’s calculations.

Insurance companies deploy delay tactics, repetitive document requests, and unnecessary examinations specifically to wear you down before you reach maximum medical improvement. Resist this pressure completely. Never settle before your doctor confirms your condition has stabilized-settling early locks in lower damages because insurers can later claim your injury wasn’t as severe as initially feared.

Use Litigation Threat as Negotiation Leverage

If negotiations stall after you’ve submitted substantial counter-evidence, filing a lawsuit within Texas’s two-year statute of limitations becomes your leverage. The threat of litigation, combined with documented evidence of economic damages and injury severity, typically accelerates settlement discussions. Venue matters significantly in Austin-area cases; Harris, Dallas, and Bexar counties trend more plaintiff-friendly than rural Texas counties. Understanding this dynamic helps your attorney position your claim effectively.

Insurance adjusters systematically undervalue claims because most injured people lack organized documentation or the willingness to fight back. They count on you settling quickly before you’ve gathered complete financial records and medical evidence. When you present comprehensive documentation and signal your willingness to litigate, settlement discussions shift dramatically in your favor.

Final Thoughts

Maximizing your personal injury settlement in Austin requires comprehensive documentation of medical expenses, meticulous wage loss calculations, and strategic negotiation backed by evidence. Insurance companies count on injured people settling quickly without organized records, but when you present itemized medical bills, physician statements about future care needs, detailed wage documentation, and employer confirmation of missed work, you eliminate their ability to dismiss your claim as inflated. The gap between median settlements of $12,281 and average verdicts of $826,892 in Texas reveals that most injured people accept far less than their cases warrant simply because they lack the documentation and negotiation strategy to push back effectively.

Professional representation fundamentally changes your settlement outcome. We at Heaton Injury Law, PLLC approach every claim with a trial-ready mindset, which means we reject lowball offers and file lawsuits when negotiations stall.

Your next step is straightforward: gather your medical records, wage documentation, and injury details, then contact us for a consultation. The two-year statute of limitations in Texas means time matters, so don’t let insurance companies wear you down through delay tactics or pressure you into settling before maximum medical improvement.

The information provided in this blog is for general informational purposes only and does not constitute legal advice. Every case is unique, and laws may vary by jurisdiction. Reading this content does not create an attorney-client relationship. For guidance specific to your situation, please consult with a qualified personal injury attorney licensed in Texas.

Artificial intelligence may have been used to assist in generating some text or images in these articles.