Meredythe | June 3, 2026 | Blog

Rideshare accidents in Austin happen more often than you’d think, and the aftermath can feel overwhelming. Insurance companies count on injured passengers not knowing their rights, which is why we at Heaton Injury Law, PLLC created this guide.

Your rideshare crash claim in Austin deserves proper handling from someone who understands both the law and what you’re going through. This guide walks you through the exact steps to protect your settlement.

Know Your Coverage After a Rideshare Crash

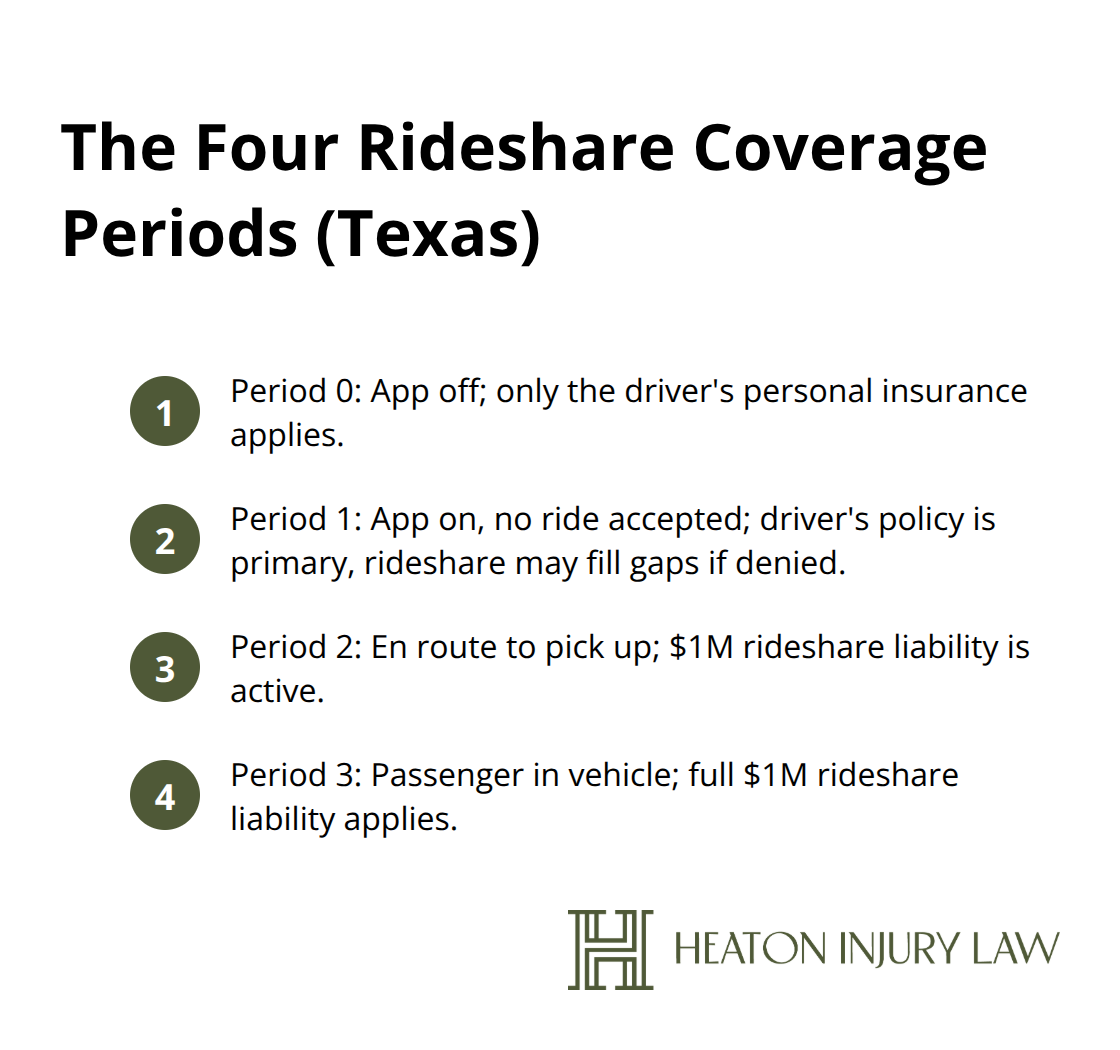

When you’re injured in a rideshare crash in Austin, the insurance picture gets complicated fast because multiple policies may apply depending on what the driver was doing at the moment of impact. Texas law divides rideshare crashes into four coverage periods tied to the driver’s app status, and which period applies directly determines how much money is available to you.

The Four Coverage Periods and What They Mean

If the driver had a passenger in the car or was actively heading to pick one up, Uber or Lyft’s $1 million commercial liability policy kicks in as primary coverage, which means substantially higher settlement potential than relying on a driver’s personal auto insurance alone. Period 3, when a passenger is in the vehicle, gives you access to that full $1 million policy. Period 2, when the driver is en route to a pickup, also activates the same $1 million coverage. Period 1, when the app is on but no ride has been accepted, typically defaults to the driver’s personal policy first, with rideshare coverage only filling gaps if that personal policy denies the claim.

Period 0, when the app is completely off, treats the crash as a standard car accident under only the driver’s personal insurance, which often means far lower coverage limits.

Capture App Evidence Immediately

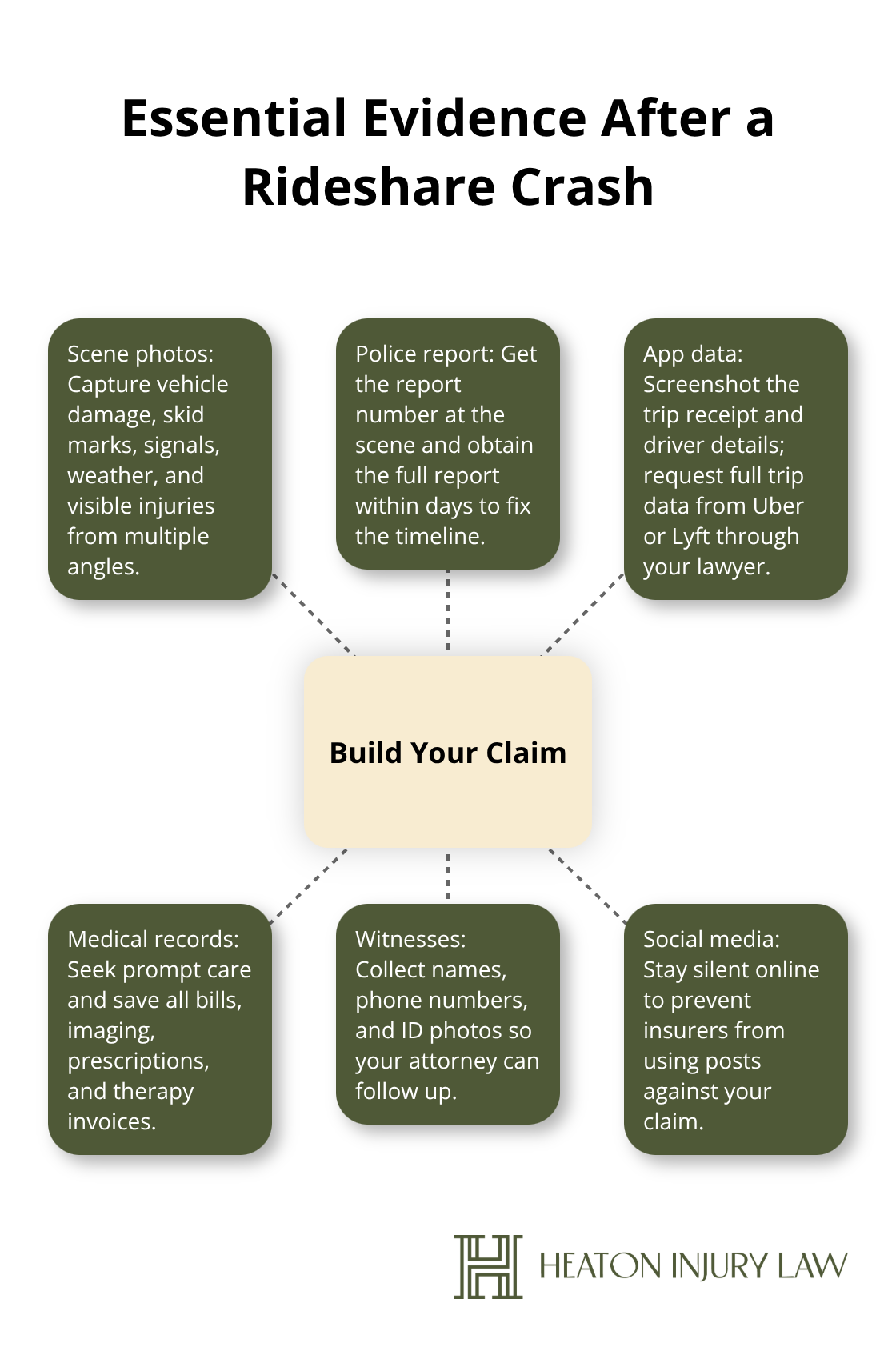

The critical mistake most injured people make is not capturing the app log immediately after the crash, because insurers will dispute which period applied if you wait. You should take a screenshot of the trip receipt and driver details right away, and request the full trip data from Uber or Lyft’s servers through your lawyer later. This single step protects your ability to prove which coverage period was active and prevents insurers from claiming the app was off when it actually was on.

Tap Into Your Own Insurance Coverage

Most victims don’t understand that their own uninsured or underinsured motorist coverage can fill gaps between what the rideshare policy pays and what your actual damages total. Your personal auto policy may have UM/UIM coverage that applies even when you’re a passenger in someone else’s vehicle, giving you a second source of recovery. Texas Department of Transportation data shows that one person is injured every 2 minutes and 6 seconds in Texas traffic crashes, yet this layered coverage approach remains underutilized.

Comparative Negligence and Fault

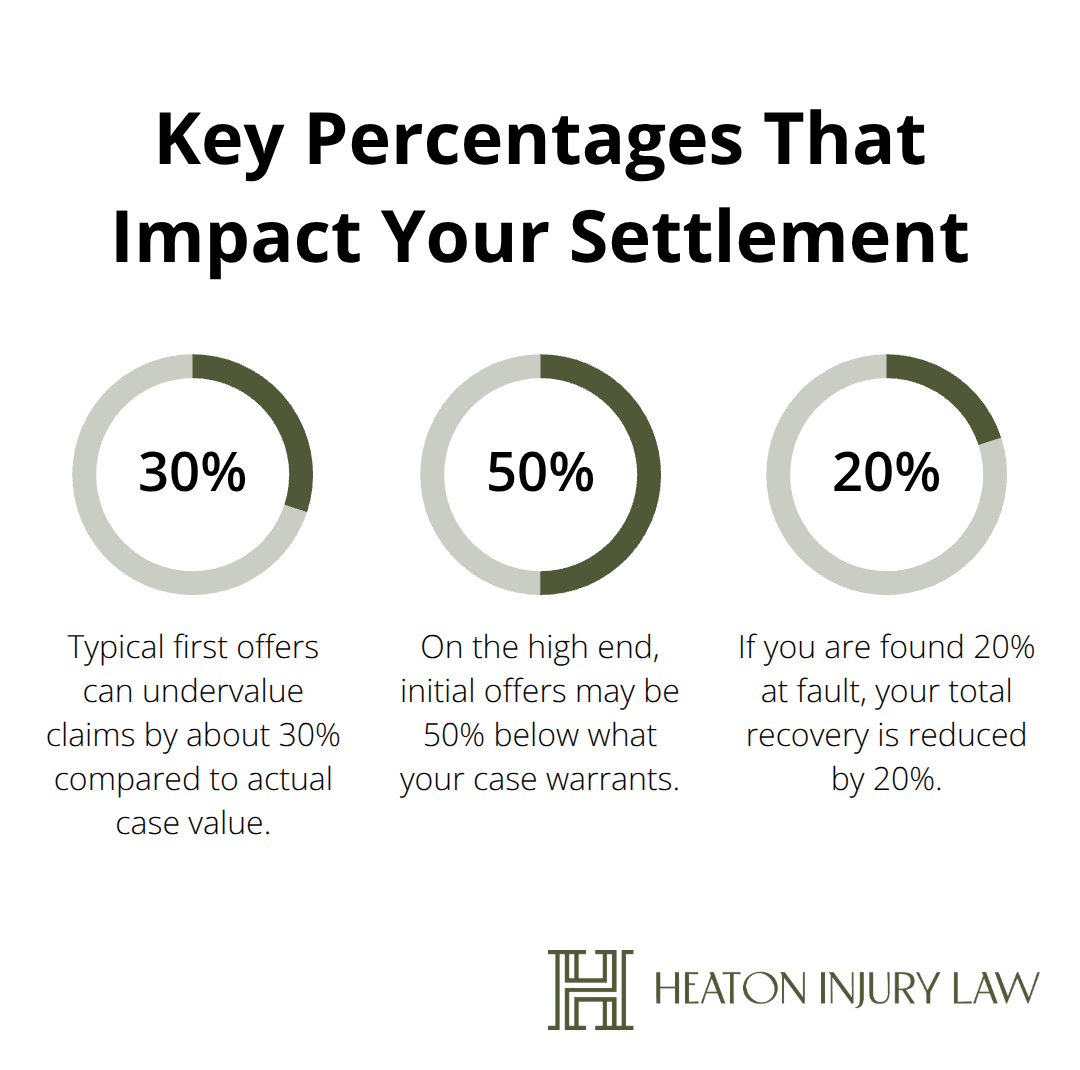

Texas follows a modified comparative negligence rule under Civil Practice and Remedies Code Section 33.001, meaning you can still recover damages even if you’re partially at fault, as long as you’re less than 51% responsible for the crash. Your recovery amount gets reduced by your percentage of fault, so if you’re found 20% at fault and your total damages are $100,000, you’d recover $80,000. This is why the exact details of how the crash happened matter enormously, and why preserving evidence like police reports, witness statements, and scene photographs immediately protects your ability to prove fault later. If you need guidance navigating these complexities, contact a skilled Austin personal injury lawyer who can help maximize your recovery.

Document Everything and Build Your Claim

The moment after a rideshare crash in Austin, most people focus on pain and getting help, which is exactly right. But the second you’re safe and receiving medical attention, the evidence-gathering window opens and closes fast. Photograph the crash scene from multiple angles, capturing vehicle damage, skid marks, road conditions, weather, traffic signals, and any visible injuries before you or anyone else moves the vehicles. Get the police report number at the scene and obtain the full report within days, as it documents the officer’s observations and establishes an official timeline that insurers respect. Collect contact information from every witness, not just those who seem friendly, and photograph their driver’s licenses or get their phone numbers so your attorney can follow up later.

Capture App Evidence Before It Disappears

Take a screenshot of the Uber or Lyft app showing the trip receipt, driver details, and pickup location before you close the app, and request the complete trip data from the company’s servers through your lawyer within the first two weeks. The National Safety Council reports that thorough documentation directly correlates with settlement outcomes because insurers have less room to dispute facts when evidence is contemporaneous and detailed. This single step protects your ability to prove which coverage period was active and prevents insurers from claiming the app was off when it actually was on.

Protect Your Claim on Social Media and in Conversations

Do not post anything about the accident on social media, send messages about your injuries to friends online, or talk about the crash in detail over email, as insurance companies actively monitor public statements and will use your own words against you to reduce your claim value. Every post, text, and comment becomes potential ammunition for the other side, so silence serves your interests far better than sharing details.

Build Your Medical Records File

Medical records become your financial roadmap for damages, so seek prompt medical attention immediately even if you feel fine, because soft tissue injuries, concussions, and internal injuries often appear days later and become harder to connect to the crash if you delay care. Collect and organize every medical bill, emergency room receipt, prescription, physical therapy invoice, imaging cost, and transportation expense to medical appointments, then calculate the total before any settlement discussion happens. Keep detailed notes on how the injury affects your daily life, work performance, and ability to exercise or socialize, because pain and suffering damages depend on documented impact.

Document Lost Wages and Future Earning Impact

Lost wages require pay stubs, tax returns, and written statements from your employer confirming the dates you missed work and your hourly rate or salary, and if the injury reduces your future earning capacity, document that too through your employer’s records and any medical restrictions on work. These records transform vague claims into concrete numbers that insurers cannot easily challenge.

Reject Lowball Settlement Offers

Do not accept the first settlement offer from the rideshare company or the driver’s insurance, as these initial offers typically undervalue claims by 30 to 50 percent because insurers bet on injured people accepting quickly rather than fighting for full compensation. An experienced Austin personal injury attorney reviews these numbers against your actual damages and negotiates aggressively to close the gap between what the insurer offers and what you truly deserve. Understanding common mistakes that reduce settlement value helps you avoid the traps that cost other victims thousands in lost recovery.

Common Mistakes That Reduce Settlement Value

Rideshare settlements collapse not because the facts are weak, but because injured people sabotage their own claims through predictable errors that insurers exploit ruthlessly. The first settlement offer you receive from Uber, Lyft, or the driver’s insurance typically sits 30 to 50 percent below what your case actually warrants, yet most victims accept within weeks because the process feels overwhelming and the initial check sounds substantial. Insurers bank on this desperation, which is why they move fast with their first offer and why you must resist that pressure absolutely.

Reject Lowball First Offers

An experienced Austin personal injury attorney reviews these numbers against your documented damages and negotiates hard to close the gap, because accepting early means leaving tens of thousands on the table. Insurance companies count on injured people not knowing their rights, which is why the initial offer arrives so quickly and sounds so final. You hold far more leverage than you realize once you understand what your actual damages total.

Stay Silent on Social Media

Social media posts, text messages to friends about your injuries, and casual emails describing the crash become evidence that insurers use against you directly, as insurance companies actively monitor public statements and deploy your own words to reduce your claim value. Every post, comment, and message becomes potential ammunition, so silence protects your interests far better than sharing details with anyone outside your legal team. Post-crash social media silence is not optional if you want maximum recovery.

Seek Medical Attention Immediately

Soft tissue injuries, concussions, and internal bleeding often appear days or weeks after impact, and if you wait too long to seek care, insurers will argue the injury resulted from something else entirely rather than the crash. National Safety Council data confirms that thorough documentation of immediate medical care directly correlates with settlement outcomes because insurers have less room to dispute causation when treatment starts quickly. Seek medical attention immediately even if you feel fine, because emergency room records, imaging reports, and physician notes create the documentary chain that proves the crash caused your injury and justifies your damages claim.

Organize Medical Records and Expenses

Collect every medical bill, prescription receipt, imaging cost, and transportation expense to appointments, then organize these records before any settlement discussion occurs. Document how the injury affects your work, daily activities, and quality of life through detailed notes, because pain and suffering damages depend entirely on showing measurable impact to a jury or insurance adjuster. The victims who recover the most money are those who treat evidence preservation with the same urgency as their medical recovery.

Final Thoughts

Rideshare crash claims in Austin involve layered insurance policies, strict deadlines, and insurers trained to minimize payouts. Navigating this alone means accepting settlements that fall short of your actual damages, missing coverage sources, and losing leverage you didn’t know you had. We at Heaton Injury Law, PLLC understand how rideshare companies and their insurers operate, and that knowledge translates directly to higher recoveries for our clients.

Your rideshare crash claim in Austin deserves representation from someone who knows the four coverage periods, understands Texas comparative negligence law, and refuses to accept lowball offers. Meredythe Heaton Wilkinson leads our firm with over 14 years of experience securing millions for injured clients across car accidents, motorcycle crashes, truck collisions, brain injuries, and rideshare incidents. We work on contingency, meaning you pay nothing unless we win.

Contact us today for a free consultation to review your rideshare accident and learn exactly what your claim is worth. We examine police reports, request trip data from Uber or Lyft, review all insurance policies, and build a strategy that maximizes your recovery. Texas gives you two years to file a personal injury claim, so reaching out now protects your rights and strengthens your position.

The information provided in this blog is for general informational purposes only and does not constitute legal advice. Every case is unique, and laws may vary by jurisdiction. Reading this content does not create an attorney-client relationship. For guidance specific to your situation, please consult with a qualified personal injury attorney licensed in Texas.

Artificial intelligence may have been used to assist in generating some text or images in these articles.