Meredythe | June 17, 2026 | Blog

A rideshare crash can leave you injured, confused, and facing mounting medical bills. Insurance companies often push settlements that don’t cover your full recovery costs.

We at Heaton Injury Law, PLLC help Austin residents understand what a fair rideshare crash settlement actually looks like. This guide walks you through the key factors that determine your claim’s value and the warning signs of inadequate offers.

How Rideshare Insurance Coverage Actually Works in Austin

Rideshare crashes involve a coverage puzzle that most injured passengers and drivers don’t understand until it’s too late. When you’re in an Uber or Lyft accident in Austin, the insurance available depends entirely on the driver’s app status at the time of impact. If the driver was online with a passenger or actively en route to pick one up, Uber’s third-party liability coverage kicks in at up to $1 million. That’s substantially higher than Texas’s state minimum of $30,000 bodily injury per person. However, if the driver was logged off the app or between rides, you’re relying on the driver’s personal auto insurance or the state minimum-a critical distinction that determines how much money is available for your claim. Insurance companies won’t volunteer this information; they’ll accept your claim under whichever policy minimizes their payout, which is why understanding app status from the start matters.

Coverage Stacking and Uninsured Motorist Protection

The real advantage for rideshare passengers lies in coverage stacking. Your own auto insurance policy may include uninsured or underinsured motorist coverage, which applies when the at-fault driver lacks sufficient insurance. A University of Chicago and Rice University study found that ride-sharing growth contributed to a 2–3% increase in U.S. traffic deaths since 2011, partly because drivers focus on apps instead of the road. In Austin’s busy corridors like Lamar, MoPac, 183 and IH-35, left-turn conflicts and rear-ends near downtown Austin frequently involve rideshare vehicles. Texas’s comparative negligence rule allows you to recover damages even if you’re partially at fault-you can collect as long as you’re less than 51% responsible. However, your percentage of fault directly reduces your recovery dollar-for-dollar, making fault determination essential. Insurance adjusters exploit unclear liability to assign you higher fault percentages, which is why scene documentation and traffic data from the crash location matter immediately.

Why Fault Analysis Determines Your Settlement Floor

Fault determination in multi-vehicle rideshare accidents requires specific evidence that adjusters will challenge. Brake-light functionality, vehicle damage geometry, electronic logging device data from commercial vehicles, and witness statements all establish negligence patterns. In rear-end crashes near retail areas like South Congress or SoCo and the Domain, insurers demand proof that the front vehicle braked suddenly or that the rear driver failed to maintain safe distance. Left-turn accidents at Lamar Boulevard and 5th Street hinge on traffic signal timing, right-of-way rules, and whether the turning driver checked for oncoming traffic. Rideshare drivers operating under app pressure may cut corners, making their negligence provable but requiring documentation collected within days, not weeks. The longer you wait to photograph skid marks, street signs, traffic signals, and nearby landmarks like the Parmer Event Center with attention to lighting conditions, the more details fade and the weaker your fault argument becomes. Insurance companies bank on this delay; they know that without contemporaneous evidence, they can dispute liability and lower their offer accordingly.

What Happens When Coverage Conflicts Arise

Multiple insurance policies create disputes over which carrier pays first and how much each owes. The rideshare company’s policy, the driver’s personal policy, your own uninsured motorist coverage, and any commercial vehicle policies (if a truck or delivery vehicle caused the crash) all compete for priority. Insurance adjusters deliberately slow-walk these determinations, hoping you’ll accept a lowball offer before coverage questions are resolved. You need clarity on which policies apply and their limits before any settlement discussion. The next section covers what your settlement should actually include-medical costs, lost income, and pain and suffering-so you can evaluate whether an offer truly compensates your losses.

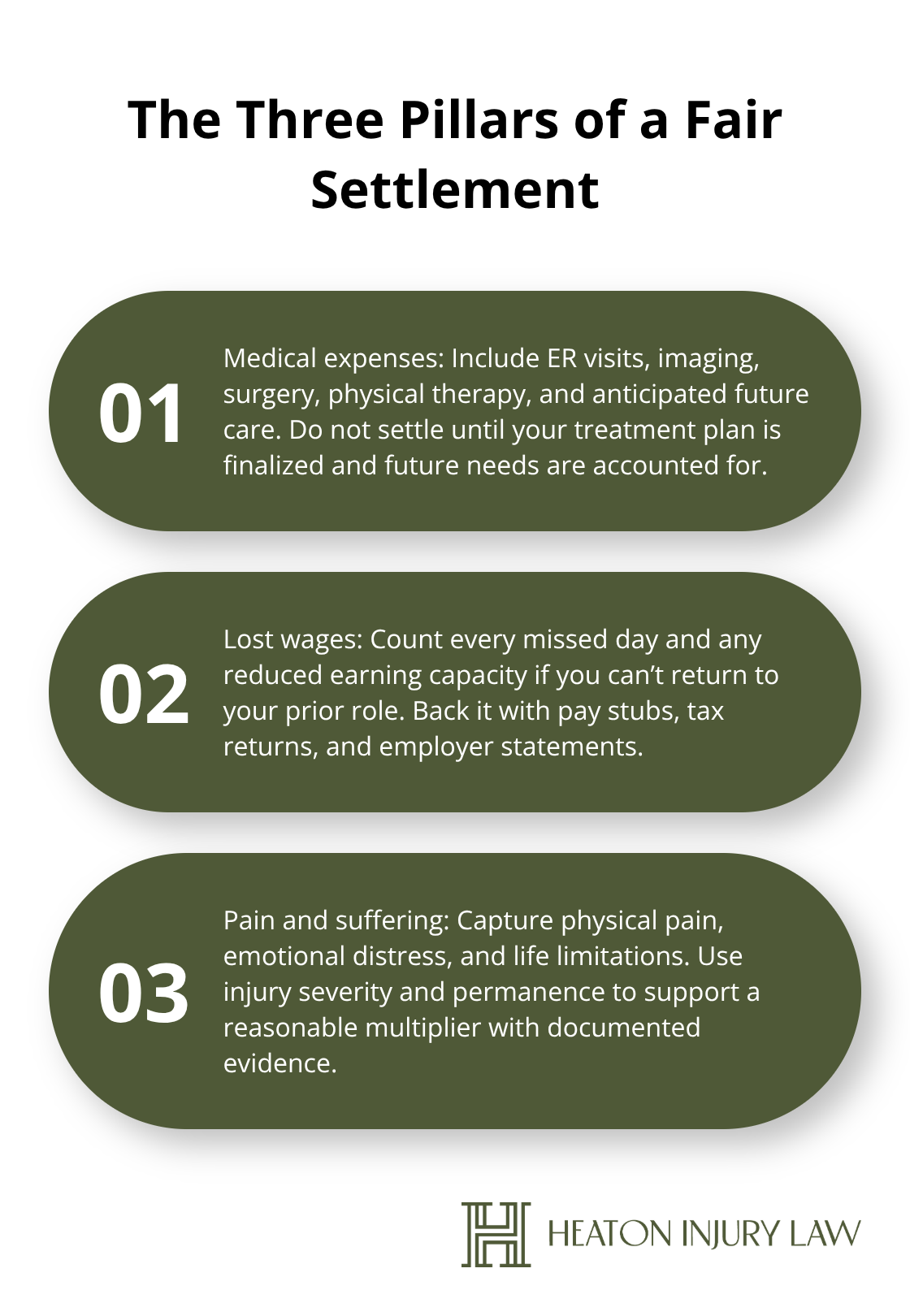

What Your Settlement Must Actually Cover

A fair rideshare crash settlement compensates three distinct categories of loss, and insurance adjusters will fight to minimize each one.

Medical Expenses Form Your Settlement Foundation

Medical expenses include emergency room visits, imaging scans, surgery, physical therapy, and any ongoing treatment your doctor prescribes. In Austin, a typical ER visit costs $2,500 to $7,500 before imaging or specialist referrals; MRI scans may average $4,200 to $5,500, and physical therapy sessions average $250 to $500 per visit. The critical mistake injured people make is accepting a settlement before their treatment plan is finalized.

You cannot know your true medical costs if you’re still in active treatment or waiting for specialist appointments-accepting early locks you into a number that won’t cover future surgery, injections, or long-term therapy.

Insurance adjusters count on this pressure. They push you to settle within weeks, before you’ve seen an orthopedist or neurologist, knowing that delayed diagnoses (like herniated discs or concussions) emerge months later when you can no longer pursue a claim. Document every appointment, imaging result, and treatment recommendation before discussing settlement numbers with any adjuster.

Lost Wages Represent Your Second Recovery Pillar

Lost wages often go underestimated in settlement negotiations. If you missed work during recovery, your settlement must include every day of lost income plus any reduced earning capacity if your injury prevents you from returning to your previous job. Request detailed pay stubs, tax returns, and written statements from your employer showing the exact dates and wages lost.

Self-employed workers should provide tax records and client invoices proving lost business income. Insurance companies frequently ignore wage loss claims without supporting documentation, so build this evidence immediately after the crash. The stronger your payroll records, the harder adjusters find it to dispute your lost income figures.

Pain and Suffering Damages Reflect Your Actual Disruption

Pain and suffering damages compensate the non-economic impact of your injury-physical pain, emotional distress, reduced quality of life, and lost enjoyment of activities. Texas law allows you to recover these damages, but they’re harder to quantify than medical bills, which is why insurers attack them aggressively. A common industry formula multiplies your medical expenses by 1.5 to 5, depending on injury severity and permanence.

Severe injuries with permanent limitations command higher multipliers; minor soft-tissue injuries receive lower ones. The Texas Transportation Institute reports that serious-injury crashes in the state totaled 15,227 in 2023 with 18,765 people seriously injured, yet settlement offers rarely reflect the actual disruption to daily life. If your injury prevents you from exercising, playing with children, or working in your previous capacity, these restrictions have monetary value.

Document them through medical records that note functional limitations and through your own journal entries describing pain levels, missed activities, and lifestyle changes. Insurance adjusters will claim your pain and suffering is worth nothing if you don’t provide this evidence.

Evaluating Whether Your Offer Covers All Three Categories

Before accepting any settlement, verify that the offer covers documented medical expenses, fully compensates lost wages with supporting payroll records, and includes a reasonable pain-and-suffering component based on your injury’s severity and permanence. Settlement offers that fall short in any of these three areas will leave you absorbing costs that should be the at-fault party’s responsibility.

Insurance companies often exploit gaps in your documentation to justify lowball offers. The next section reveals the specific red flags that signal an inadequate settlement-warning signs that should trigger immediate caution before you sign anything.

Red Flags in Settlement Offers You Should Never Ignore

The Lowball Opening Offer Trap

Insurance adjusters deploy a three-stage strategy to minimize what you receive: they lead with a lowball figure, pressure you to accept it quickly before your case is fully documented, and bury coverage limitations in dense policy language. The first offer from an insurance company is almost never their best offer-it’s a negotiating anchor designed to be 40 to 60 percent below what your claim actually warrants. An adjuster calling within days of your crash with a settlement number signals that they’ve completed minimal investigation and are betting you’ll accept out of financial desperation.

This tactic works because injured people face immediate pressure: medical bills arrive, rent is due, and lost wages create genuine hardship. Adjusters know this and weaponize urgency. They’ll claim your case is straightforward, that they’re offering fair value, and that delays only cost you money in legal fees. A fair settlement requires completed medical treatment, documented wage loss, fault analysis with scene evidence, and a clear understanding of all available insurance coverage. Accepting an offer before these elements are in place means you’re signing away claims for costs you haven’t yet incurred and damages you haven’t yet quantified.

Settlement Pressure Without Legal Review

The second red flag appears when an adjuster pressures you to sign a settlement agreement without allowing time for independent legal review. Settlement documents contain release language that permanently waives your right to pursue additional claims, even if new medical issues emerge months later. Herniated discs, concussions, and chronic pain conditions frequently surface after initial treatment ends; accepting a settlement before these develop means you absorb the cost entirely.

Insurance companies insert exclusion clauses and coverage limitations into settlement terms specifically to avoid liability for future treatment. A policy might exclude pre-existing conditions, cap mental-health coverage, or deny payment for certain specialists-and adjusters will point to these exclusions as justification for lower offers without explaining how they reduce your actual recovery. Demand a written explanation of every coverage limit and exclusion before any discussion of settlement numbers.

Hidden Exclusions and Coverage Gaps

Request the complete policy documents, not summaries. Ask specifically which medical providers are in-network versus out-of-network, because out-of-network treatment often triggers higher out-of-pocket costs that reduce your net recovery. Insurance adjusters count on you not reading the fine print; they’re betting you’ll sign the settlement release without understanding that you’ve forfeited claims for future treatment, lost earning capacity, and permanent disability.

Final Thoughts

A rideshare crash settlement in Austin requires you to verify that your offer covers all documented medical expenses, fully compensates lost wages with supporting payroll records, and includes pain-and-suffering damages proportional to your injury’s severity. Insurance adjusters deliberately move fast, knowing that injured people face immediate financial pressure and incomplete information about their injuries. They count on you accepting an offer before you understand the full scope of your damages or the coverage available to you, and a settlement signed too early locks you into a number that won’t cover future surgery, specialist care, or complications that emerge months later.

Professional legal review protects you from these tactics. An attorney experienced in rideshare crashes understands how coverage stacking works, how to identify all liable parties, and how to challenge insurance company exclusions that reduce your recovery. We at Heaton Injury Law, PLLC prioritize your complete recovery, not speed-we wait until your diagnosis and treatment plan are finalized before making any demand, because that’s when your claim’s true value becomes clear.

Contact us for a free consultation to review any settlement offer you’ve received or to discuss your rideshare crash settlement Austin from the beginning. We represent clients on contingency, meaning you pay no fee unless we recover money for you, and court costs come from your recovery and are explained in writing before any settlement.

The information provided in this blog is for general informational purposes only and does not constitute legal advice. Every case is unique, and laws may vary by jurisdiction. Reading this content does not create an attorney-client relationship. For guidance specific to your situation, please consult with a qualified personal injury attorney licensed in Texas.

Artificial intelligence may have been used to assist in generating some text or images in these articles.